Why focus on lithium batteries in North America?

With the rise of the energy transition, the electric vehicle (EV) industry is booming as an alternative to internal combustion vehicles, one of the major sources of carbon emissions. The year-on-year increase in EV vehicle sales has resulted in strong demand for power batteries. The resilience of the grid is being challenged as the proportion of sustainable energy in each country keeps increasing such as wind and solar. As a result, energy storage facilities, especially battery storage, are expanding at an unprecedented rate.

For the United States in particular, the strategic focus on the lithium-ion battery industry has been underway since the Obama administration. In the face of the challenges of climate change and the volatility of global energy markets, strengthening the development of the lithium industry has become one of the key strategies for the United States to ensure energy security and promote a green, low-carbon transformation of the economy.

Currently, more pioneering companies in the lithium-ion battery industry chain, from raw material minerals to the manufacturing of battery cells, are located outside of North America. In particular, lithium-ion battery cell manufacturing capacity is highly concentrated in the Far East. In terms of raw materials, for lithium alone, North American reserves will struggle to support future demand (the United States and Canada's proven reserves account for only about 7.25% of the global total, according to the U.S. Geological Survey). Lithium refining capacity in North America is also limited, making rapid growth in the mining and primary raw materials sector less likely in the short term. Furthermore, North America lacks an industrial base in battery manufacturing.

However, the federal government, which is committed to achieving industrial autonomy and re-industrialisation, has chosen to balance the price advantage of imported products through political and economic means and has vigorously supported domestic and foreign companies to invest in America. The expected strong consumption power in the North American market plus the relevant policies reshape the global lithium battery market and industry chain layout, which is particularly noteworthy.

Policy-driven battery industry chain flourishing

Since the Obama administration approved federal funds to provide large-scale subsidies to A123, a startup specializing in lithium iron phosphate batteries, the United States has started to steer the progress of the domestic battery industry through policy guidance. However, A123 was eventually abandoned by investors due to profitability difficulties caused by technology that was ahead of market demand. Occasional battery failures even led to its fall into the depths. After the U.S. government abandoned its bailout, A123 was reorganised in bankruptcy and acquired by China's Wanxiang Group.

In the rise of electric vehicles led by Tesla, Chinese battery manufacturers such as CATL, BYD and upstream battery material manufacturers have also gradually risen and gained an advantageous position in the middle link of the global industrial chain. At the same time, the United States in the field was lagging. According to SMM statistics, in 2021, the global production of lithium-ion batteries for electric vehicles was approximately 80% from China, the same year the United States capacity was only about 6%.

The U.S. government for the protection of domestic industry and other factors, began to re-launch lithium-ion battery manufacturing and its industrial chain by large-scale policy support. The Inflation Reduction Act (IRA) is the most iconic one promulgated by the Biden government in 2022.

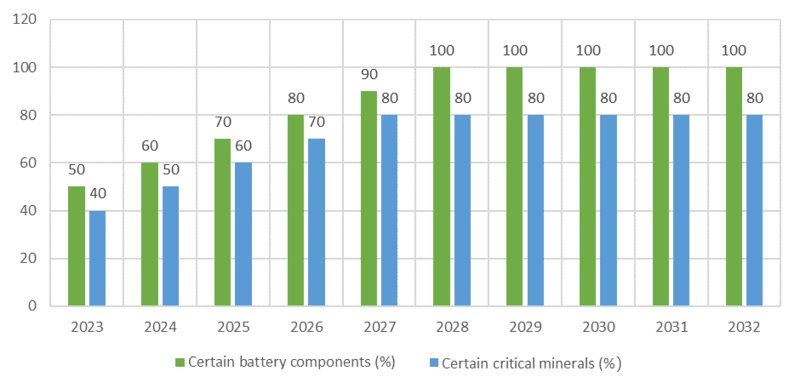

The bill's subsidies for the North American lithium-ion battery and electric vehicle industry fall into two main categories. The first subsidy with a total of $7,500 is for consumers who purchase eligible electric vehicles, of which a $3,750 tax credit can be allocated as the battery components manufactured or assembled in North America meet or exceed a specified value. The other $3,750 tax credit for consumers can be secured, as the battery contains a specified percentage of certain critical minerals extracted or processed in the United States or an FTA country. The specific percentage requirements are increasing year by year as follows.

Figure 1. Value proportionality requirements for IRA tax credits

Source: U.S. Federal Government, SMM

The second component is a tax credit for manufacturers of battery cells or packs located in the United States, which is not to exceed $35 or $10 tax credit per kWh, respectively.

On this basis, the U.S. Department of the Treasury has imposed country-specific requirements on tax credits to exclude key competitors. There is no tax credit eligibility for battery components manufactured or assembled in a foreign entity of concern (FEOC) from 2024 onwards, and no tax credit eligibility for critical minerals extracted, processed or recycled in a FEOC from 2025 onwards.

At the same time, the Department of the Treasury, most state governments, and local governments offer project-based subsidies or financing loans for battery plants. The subsidy includes but is not limited to, start-up financing, capital and infrastructure support during construction, performance-based incentives, job creation-based incentives, and free labour training support. Such support is attractive to battery manufacturers, especially start-ups that lack initial capital. For example, at Panasonic's cell plant in Kansas, the state has allocated $140 million directly to the battery plant and $10 million in labour mobilisation. At the same time, governments are providing tax incentives totalling $156.3 million, of which $85 million will be used for local water and transport upgrades, with the remainder to be used as performance-based tax incentives over the next three decades.

As an important partner of the United States in the automotive industry chain, Canada has also implemented support and subsidies for projects related to the battery industry within its borders. After Northvolt agreed to choose Montreal as the location of its first gigafactory in North America, the Canadian government immediately announced that it would subsidise it in line with the IRA. The Quebec government has committed up to C$2.9 billion to secure the deal, while the federal government will contribute up to C$1.34 billion, which is around 41.4% of its total investment. Meanwhile, one of Canada's largest pension groups has invested C$400 million into it, giving the plant a strong capital base and greatly facilitating political and business relations.

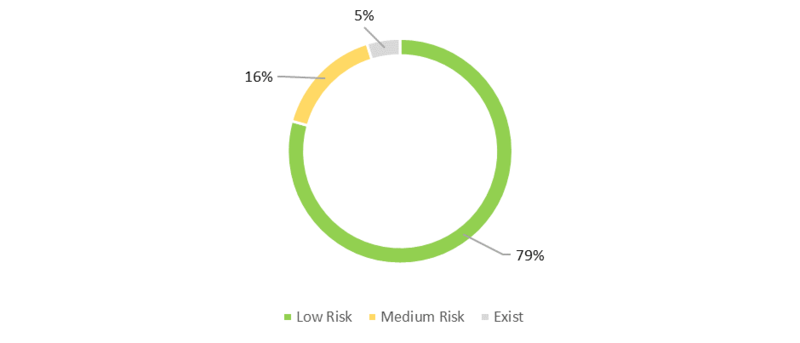

Earlier SMM posted an analysis of the lithium-ion battery industry in Europe. Compared to similar projects in Europe, we can see that with the support of multi-level subsidies, the lithium-ion battery programs in North America have a higher proportion of low-risk projects.

Figure 2. Proportional distribution of capacity risk in North America (based on estimated capacity in 2030)

Source: SMM

Broad prospects for lithium batteries in North America

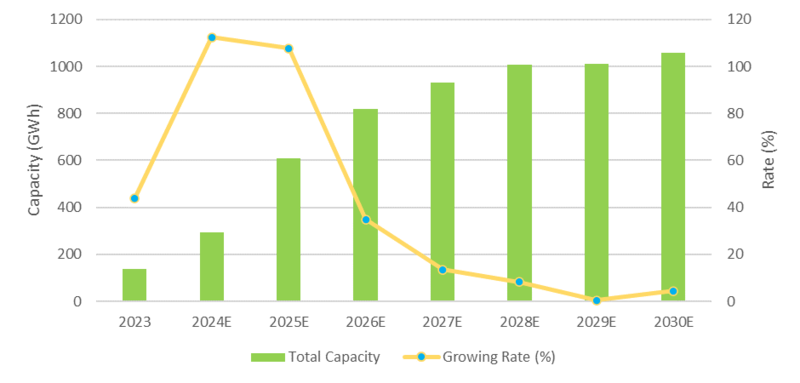

With the growing domestic EV & BESS market and diverse policy support, North American lithium-ion battery capacity is expected to increase rapidly. According to SMM data, lithium-ion battery capacity in North America will exceed 1 TWh in 2028. Capacity will increase by approximately 859.5 GWh over the five-year period from 2023 to 2028, which equates to a nearly tenfold increase.

Figure 3. Lithium battery capacity for 2030 in North America

Source: SMM

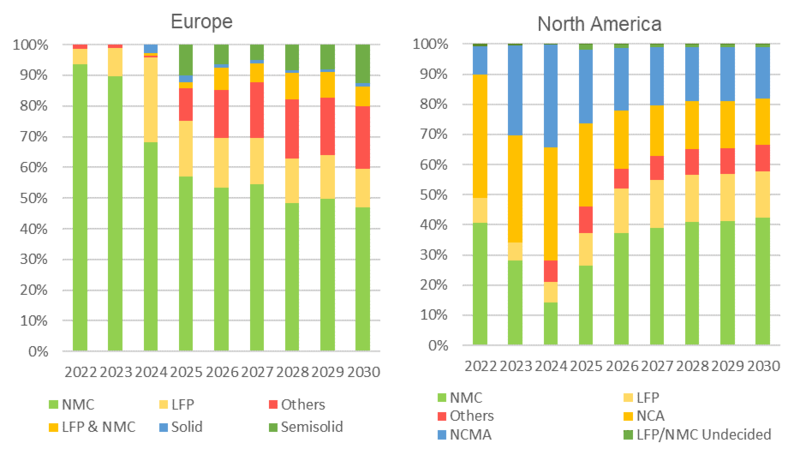

Unlike Europe, North American capacity is much more diverse, with both LFP and NCMA accounting for significant shares, even exceeding NMC's total capacity in some years. In contrast, the capacity share of NMC batteries in Europe is way ahead. North America's solid-state lithium battery capacity layout is more aggressive and far better than only a small number of pilot plants or small-scale solid-state lithium battery projects in Europe. It is reviewed that North American companies are more aggressive on advanced technologies and immature components when they are investing in the battery industry. Instead, Europe prefers to continue on their classic route of using NMC as cathode material on power batteries.

Figure 4. Schematic representation of battery capacity by type

Source: SMM

Conclusion and beyond

The future of the North American lithium battery industry is generally bright. Given the pressures of the energy transition in the United States and Canada, the rapid development of EV and ESS facilities could drive huge demand for lithium-ion batteries. Compared to full import, supporting domestic production and industry chain from the perspective of industrial competition is helpful to boost the domestic manufacturing industry. At the same time, lithium-ion batteries and their upstream & downstream industries can also provide more employment opportunities in the region.

Yet uncertainties also remain, particularly concerning competition in international markets and policies. Currently, the small capacity that has been built in North America puts it at a disadvantage in comparison with countries such as China, in terms of technology, cost and economies of scale. Meanwhile, although the U.S. electric vehicle market share rose to 7.6% in 2023, the growth rate and investor enthusiasm for the electric vehicle industry have already begun to slow down. For the sparsely populated and vast North American continent, an insufficient number of charging facilities will dampen consumers' enthusiasm for electric vehicles for quite some time to come. Even though policy subsidies and support can somewhat attenuate the cost disadvantage of domestic products, the sustainability of the policies remains to be seen. Based on the above factors, it cannot be ruled out that the United States and Canada will introduce more support policies in the future.

For companies looking to enter the North American market and consider investing in local battery manufacturing capacity, the balance between the subsidies and the higher cost of production in North America should be fully considered. It should also be noted that the localisation rate requirement for subsidies such as the IRA Act is increasing annually and will end in 2030-2032. The only concern arising would be whether or not current and potential investments are still cost-effective.

Author: Yaoning Liu | Analyst Associate, Lithium Battery | London Office, Shanghai Metals Market

Email: edenliu@smm.cn