SMM, December 18: Since December 16, SHFE lead main contract prices have been climbing continuously, reaching a peak of 17,775 yuan/mt upon opening on the morning of December 18. However, in the afternoon, as bullish funds collectively exited the non-ferrous metals sector, coupled with the lifting of the heavy pollution orange alert in Anhui, the previously surging lead prices plummeted. By the close of the daytime session, SHFE lead main contract prices fell by 1.2%, settling at 17,295 yuan/mt.

In terms of spot prices, according to SMM spot quotations, as of December 18, SMM 1# lead ingot spot prices rose to 17,300–17,450 yuan/mt, with an average price of 17,375 yuan/mt, marking a three-day consecutive increase and hitting a new high since late August.

》Click to view SMM lead product spot prices

From a fundamental perspective, on the supply side, as northern China enters the heating season, smoggy weather has occurred frequently. According to SMM, based on joint consultations by the Ministry of Ecology and Environment, it is predicted that starting from December 16, due to widespread stable weather conditions in northern China and the southward movement of cold air, regions north of the Huai River and the western Jianghuai area will experience moderate to severe pollution. Consequently, 26 cities across six provinces, including Anhui, Henan, Shaanxi, Zhejiang, Shandong, and Shanxi, issued heavy pollution weather alerts, and "suspension of work, production, and transportation" phenomena emerged nationwide. This large-scale suspension of work and production has had widespread impacts, halting construction sites, pausing production activities in numerous factories, and disrupting logistics and transportation. According to an SMM survey on December 17, secondary lead smelters in Shandong were in a state of shutdown, with enterprises estimating that this suspension would affect production by approximately 2,000 mt. Similarly, secondary lead smelters in Anhui reported on December 16 that production needed to be halted in response to the weather alert, with resumption dates depending on weather changes. Production is expected to decline by over 2,000 mt/day.

However, according to the latest updates, SMM has learned that the heavy pollution orange alert in Anhui has been lifted. Following the alert's termination, SMM's survey revealed that some secondary lead smelters in Anhui, which had shut down furnaces two days prior, would require half a month to resume operations. Other smelters have already begun raising temperatures and are expected to gradually produce lead overnight. In the short term, secondary lead supply may remain tight.

Meanwhile, SMM also investigated the neighboring Shandong province, where local secondary lead smelters reported that they had not yet received notification of the alert's termination and were still in a state of shutdown and heat preservation.

On the demand side, according to recent SMM surveys, as the year-end approaches, some large battery producers are ramping up production to meet annual targets, leading to an overall improvement in the operating rate of lead-acid battery manufacturers and boosting downstream operations.

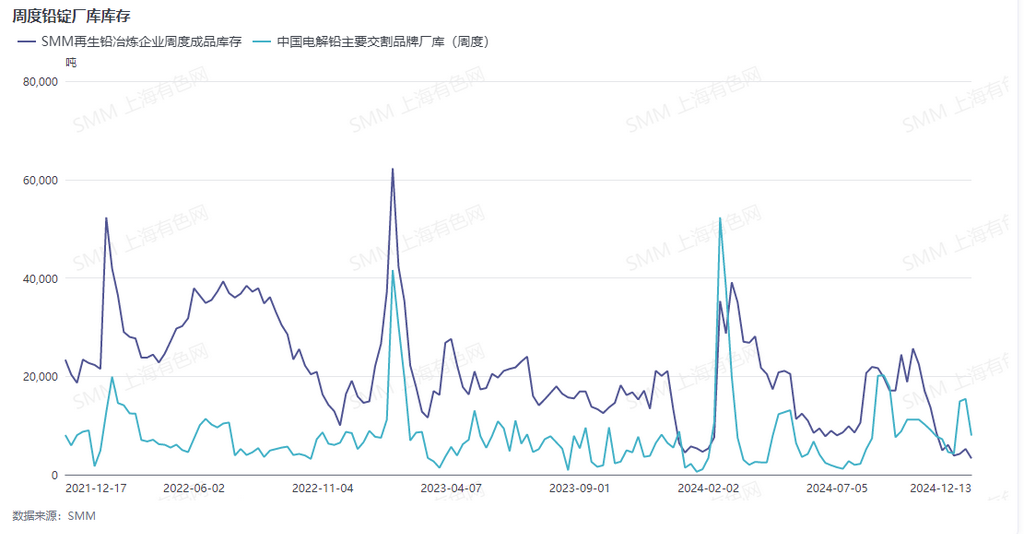

Notably, weekly finished product inventories at secondary lead smelters recently hit a historical low. Specifically, according to recent SMM surveys, due to limited battery scrap availability and strong sentiment among suppliers to hold back cargoes, smelters faced poor raw material arrivals. Additionally, with relatively favorable secondary lead profits in early December, smelters significantly increased production and resumed operations, rapidly consuming raw material inventories. Currently, SMM data shows that raw material inventory days at secondary lead smelting enterprises have fallen below the dynamic average level.

》Click to view the SMM database

Against the backdrop of tight raw material supply, multiple secondary lead smelters have shown signs of declining production since last week. Coupled with the five-day consecutive decline in lead prices last week, downstream battery enterprises have become more active in restocking and purchasing at lower prices. Finished product inventories at enterprises have also declined significantly, with weekly finished product inventories at secondary lead smelters hitting a historical low on December 13. Meanwhile, secondary lead smelters are stockpiling scrap ahead of the Chinese New Year, and battery scrap prices are more likely to rise than fall. Tight supply continues to support prices, further bolstering lead prices.

Additionally, last week, the operating rate of primary lead and in-plant inventories of major delivery brands also showed a downward trend. With supply tightening across the board, and as the New Year holiday approaches, pre-holiday stockpiling expectations persist. Some large enterprises are ramping up production to meet year-end targets. Against the backdrop of tight supply and increasing demand, lead prices remain supported at the bottom.

However, it is worth noting that with the recent continuous expansion of the SHFE/LME lead price ratio, attention should be paid to the potential opening of the refined lead import window. If the refined lead import window opens, it may alleviate the tight domestic lead supply. Additionally, attention should be given to heavy pollution weather conditions across various regions, which may disrupt the lead supply side.