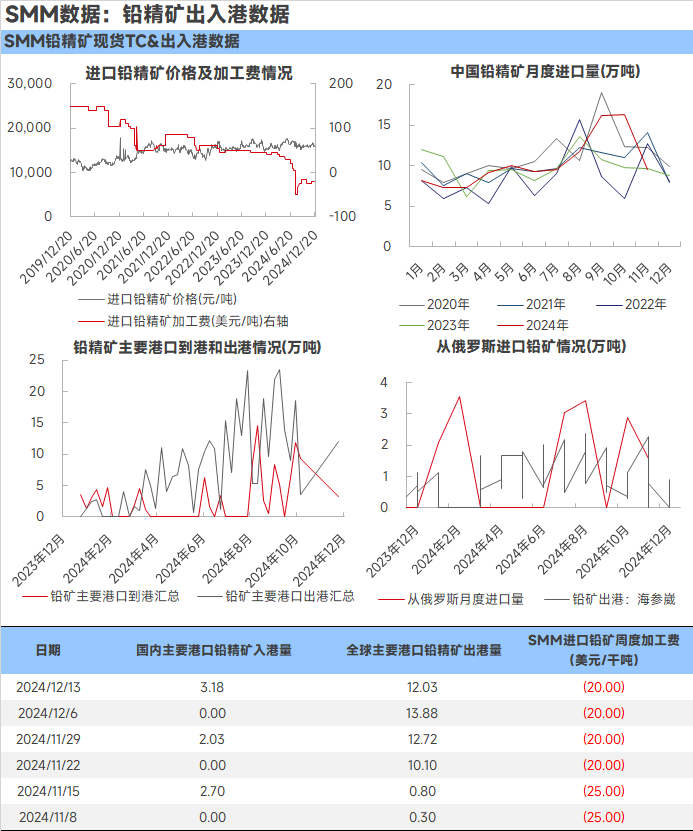

According to the latest customs data, the import volume of lead concentrate in November 2024 reached 94,900 mt, with cumulative imports of lead concentrate in 2024 totaling 1.1444 million mt (metal content), up 4.22% YoY. By country, Peru, Russia, and Australia were the main sources of lead concentrate imports in November. Additionally, the import volume of silver concentrate in November was 143,000 mt, up 6.72% MoM. In mid-to-late December, the trading activity in the ore market remained subdued. This week, the SHFE/LME price ratio continued to rise, while the supply of imported ore remained tight, leading to a slight decline in TC quotations. As year-end approaches, smelters generally showed low purchasing interest and still preferred polymetallic ores containing silver, copper, lead, and zinc, aiming for higher by-product revenues. In the domestic market, crude lead production in Hunan was temporarily halted for nearly 10 days due to environmental protection-driven production restrictions. However, the TC quotations for lead concentrate in the region did not show significant fluctuations as a result.