SMM, December 26:

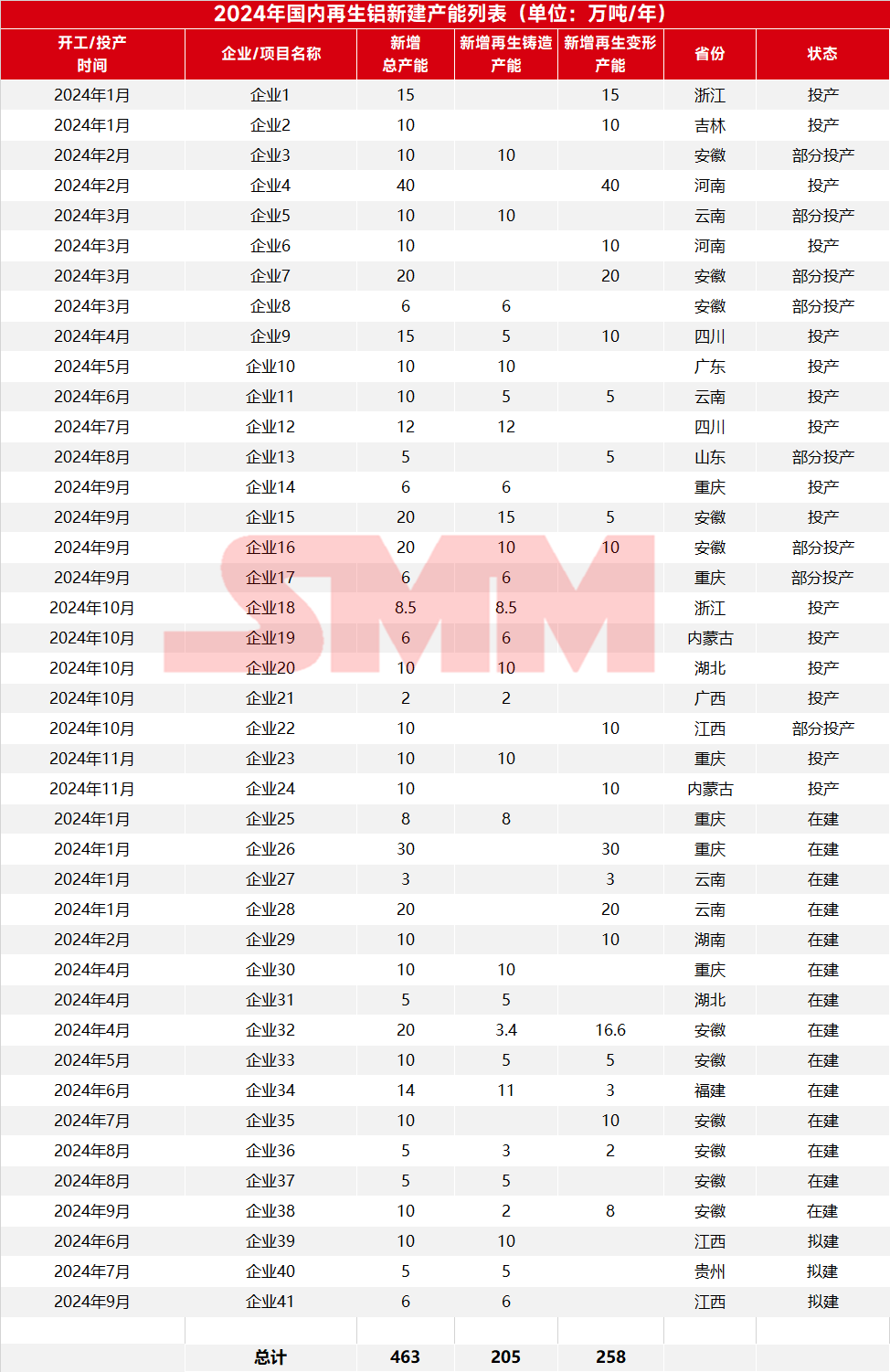

According to SMM statistics, 41 new and under-construction secondary aluminum projects are expected to be added in China in 2024, with a total capacity of 4.63 million mt. Among them, the new capacity for secondary cast aluminum alloy is approximately 2.05 million mt, while that for secondary wrought aluminum alloy is about 2.58 million mt.

The specific new capacities and project operating conditions are summarized by enterprise and product structure as follows:

Focusing solely on secondary cast aluminum alloy, SMM statistics show that 28 new and under-construction secondary cast aluminum alloy projects are planned in China for 2024, involving a capacity of 2.05 million mt. Among these, 16 projects are expected to be operational, with an actual new capacity of 1.32 million mt this year. Compared to the 1.88 million mt capacity in 2023, the pace of capacity expansion continues to slow. Most of the new capacity this year is expected to commence operations in H2, with only 460,000 mt starting in H1, accounting for about 35% of the new capacity.

The secondary cast aluminum alloy capacities completed in 2024 are as follows:

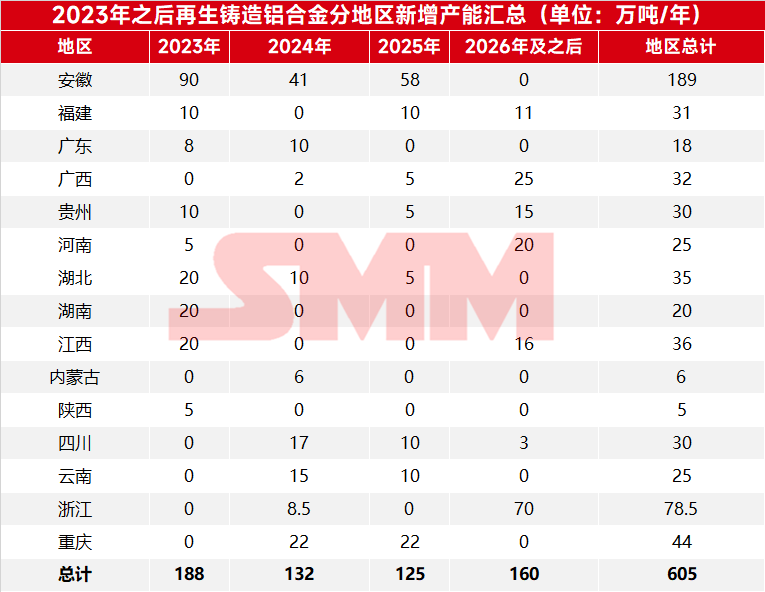

In terms of the regional distribution of new capacity, Anhui, Sichuan, and Yunnan rank as the top three, with new capacities of 410,000 mt, 170,000 mt, and 150,000 mt, respectively, in 2024. The specific regional distribution is as follows:

From the perspective of enterprises, more than half of the new capacity is contributed by leading enterprises. Their new production sites in Yunnan, Hubei, Anhui, and other regions will further expand their market coverage and optimize their product structures.

Although the expansion of secondary cast aluminum alloy projects has slightly slowed this year, the weak end-use consumption and the release of new capacity have further exacerbated the industry's oversupply, intensifying market competition. Meanwhile, the domestic aluminum scrap supply remains tight, and the overall replenishment from imported aluminum scrap is limited due to inverted domestic and international prices, failing to meet the rapidly growing downstream demand. This has led to persistently high raw material prices, reducing profits or even causing losses for secondary aluminum enterprises, thereby affecting their production enthusiasm and limiting the improvement of the industry's operating rate. By 2025, the release of new secondary aluminum alloy capacity is expected to continue at a slow pace. Additionally, due to policy adjustments and raw material constraints, some capacities may exit the market.