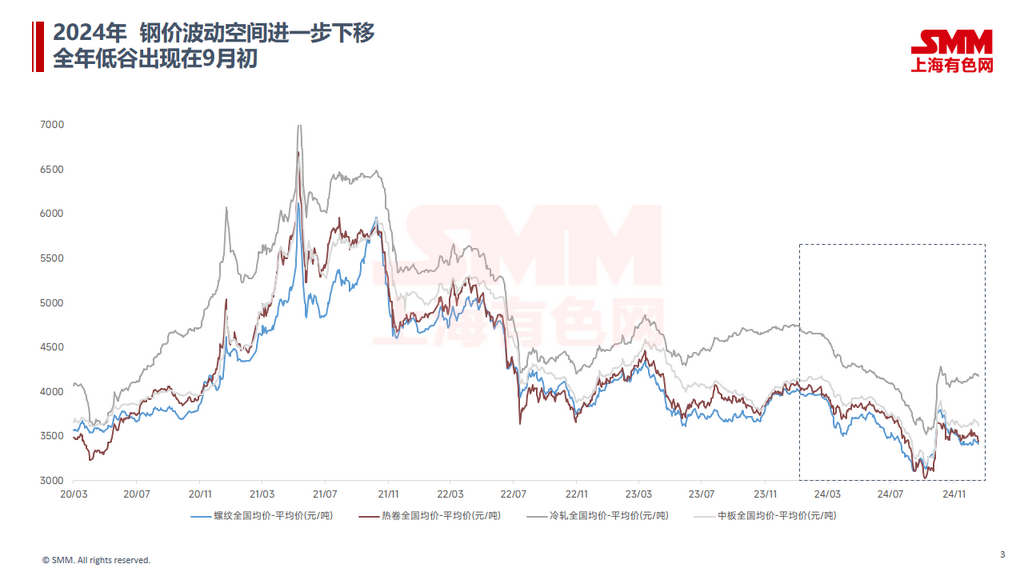

In 2024, China's steel prices experienced further downward fluctuations, with the annual price low occurring in early September. In Q4, driven by the implementation of multiple favourable stimulus policy packages, steel prices rebounded significantly. However, due to macro policies falling short of expectations, market confidence was hit again, leading to a pullback in steel prices from high levels.

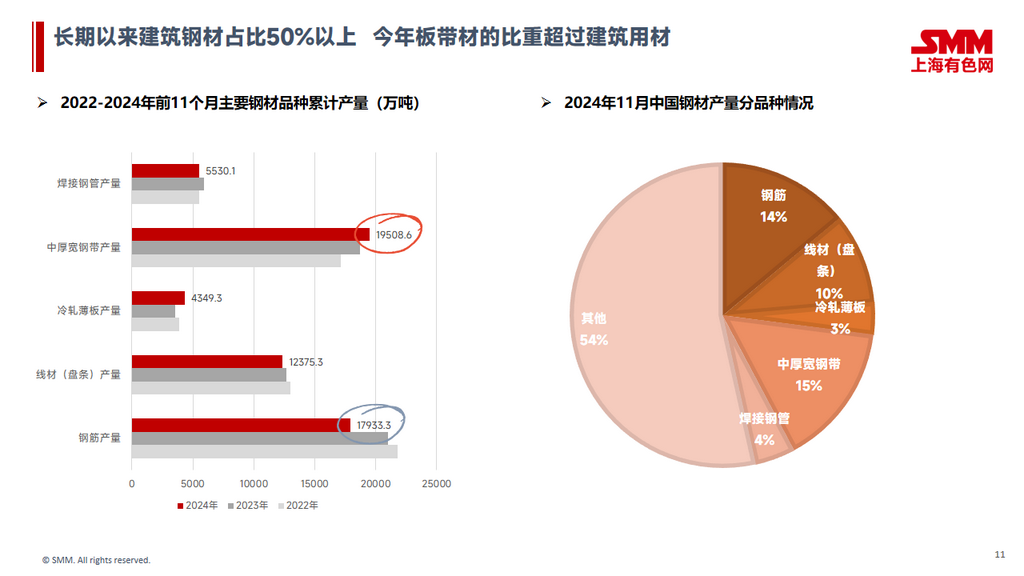

In 2025, China's steel market is expected to see increases in both supply and demand. However, the issue of overcapacity will persist, and the imbalance in overcapacity for products such as sheets & plates may further intensify.

In 2024, six new hot-rolling production lines were commissioned domestically, with a total capacity of approximately 18.8 million mt. By region, among the new production lines in 2024, east China and north China added three and two lines, respectively, while southwest China added one line.

In the medium and long-term, there are still 14 production lines domestically, with a total capacity of 38.74 million mt, awaiting commissioning. The capacity for sheets & plates is expected to see significant growth in the future.

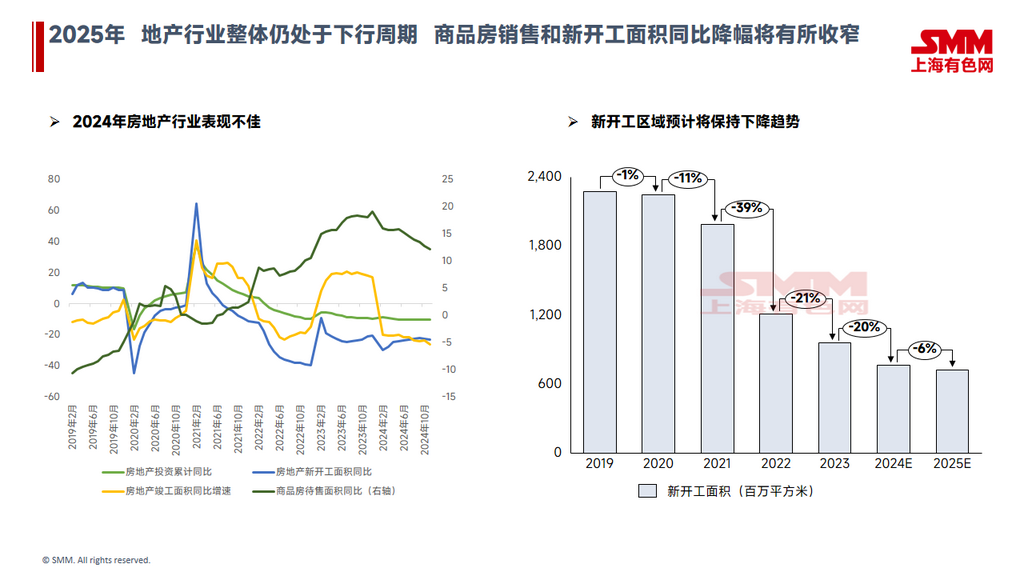

From the demand perspective, in 2025, the real estate sector is expected to remain in a downward cycle overall. However, supported by real estate-related policies, the YoY decline in commercial housing sales and new construction areas may narrow.

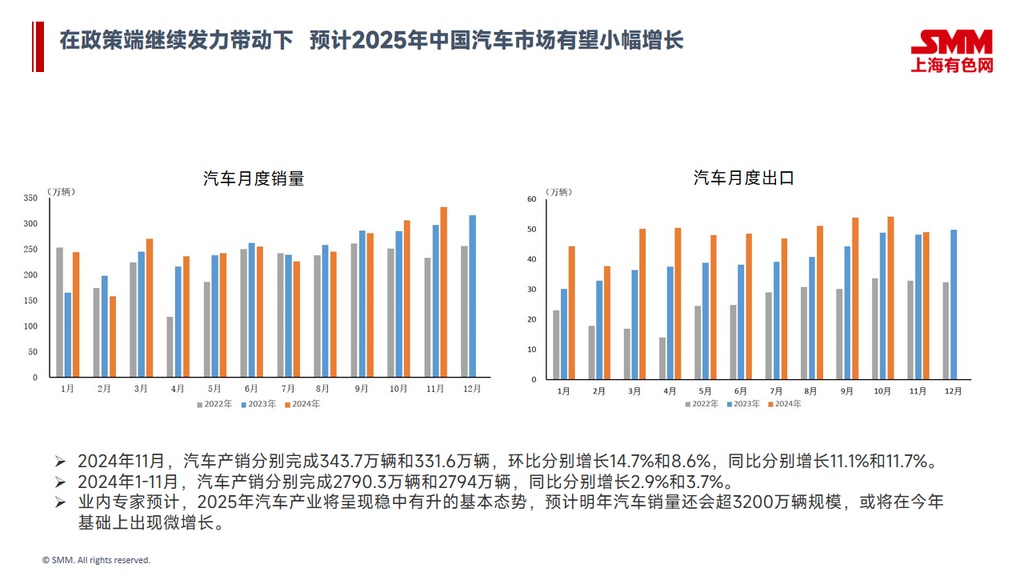

In the automotive industry, from January to November 2024, China's automobile production and sales reached 2,790.3 thousand units and 2,794 thousand units, respectively, up 2.9% and 3.7% YoY. According to industry experts, the automotive industry is expected to show steady growth in 2025.

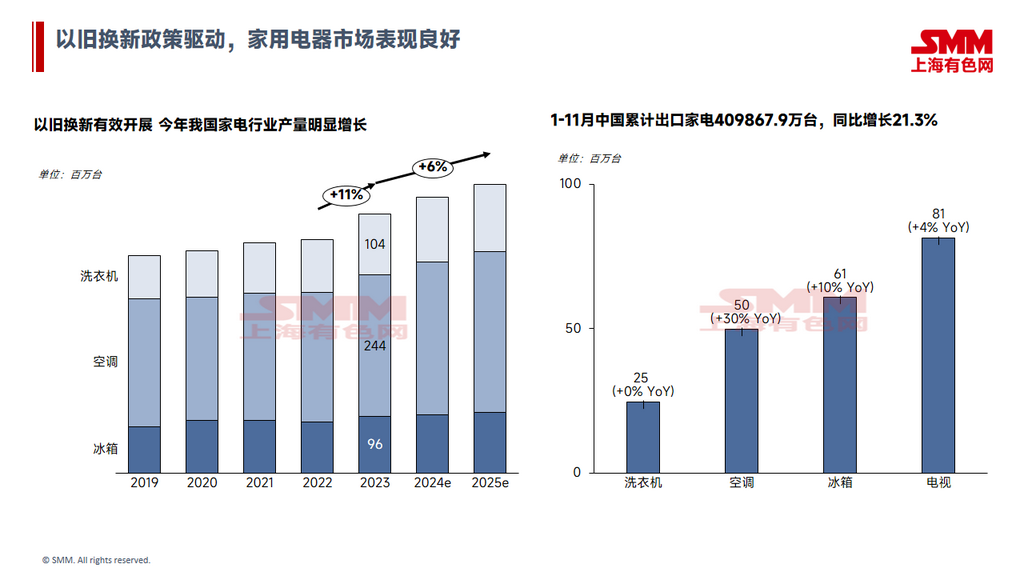

In the home appliance industry, driven by trade-in and real estate-related policies, the market performed well this year. Demand in the home appliance industry is expected to further gain momentum in 2025.

Additionally, in manufacturing sectors such as machinery and shipbuilding, there is potential for slight demand growth in 2025.

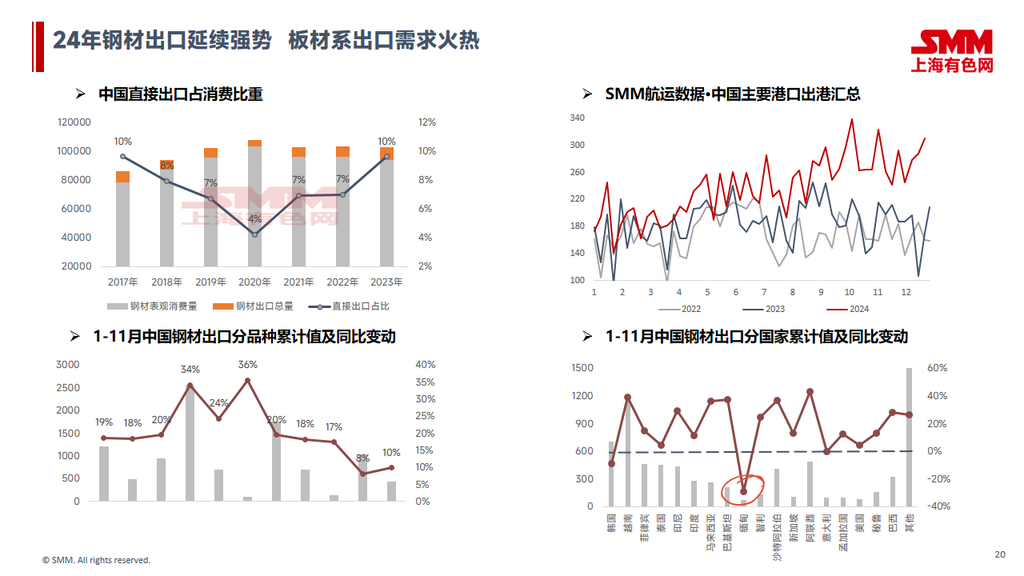

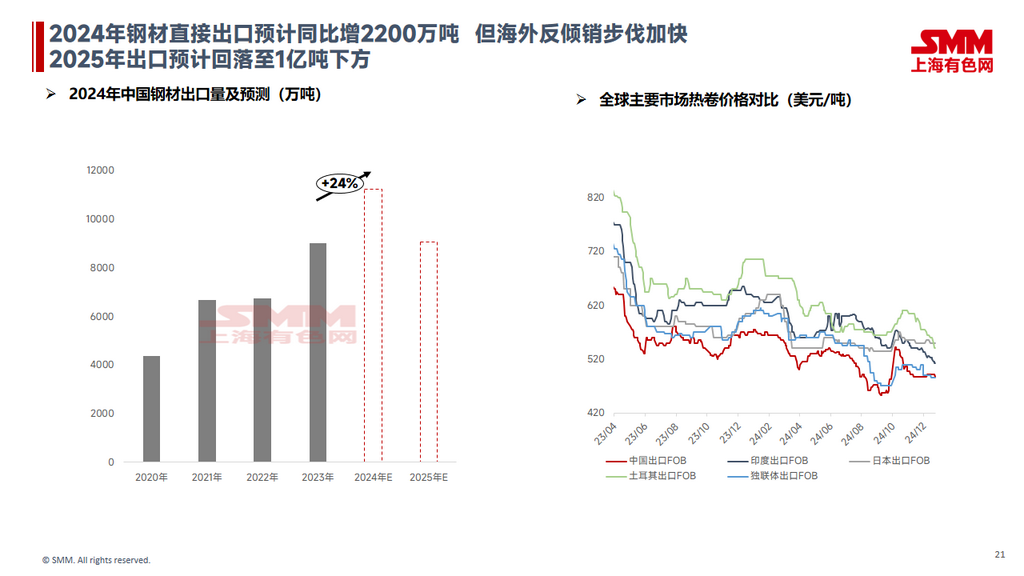

On the export front, steel exports remained strong in 2024, with robust demand for sheets & plates. Steel direct exports are expected to increase by approximately 22 million mt YoY in 2024. Looking ahead to next year, considering the accelerated pace of anti-dumping measures overseas and increased uncertainties in domestic and international policies, steel direct exports in 2025 are expected to fall below 100 million mt YoY.

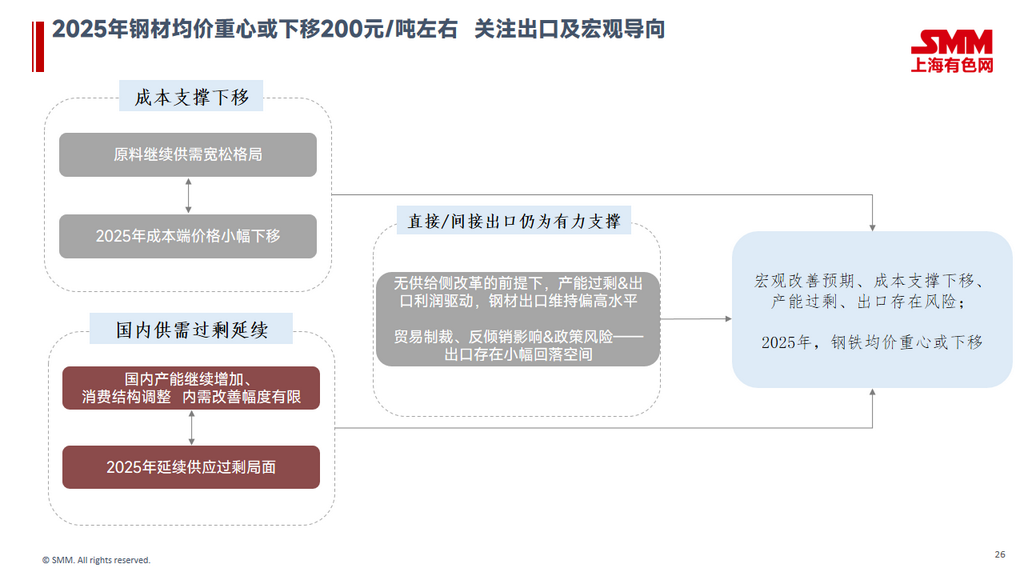

Looking ahead to 2025, raw materials are expected to maintain a loose supply and demand balance, with cost-side prices likely to edge down. Considering the continued surplus in domestic steel supply and demand, especially the significant pressure on sheets & plates, coupled with the risk of declining exports, the average steel price center in 2025 is expected to follow costs downward. Attention should be paid to exports and macro policy directions.