》View SMM Metal Quotes, Data, and Market Analysis

》Subscribe to View Historical Price Trends of SMM Metal Spot

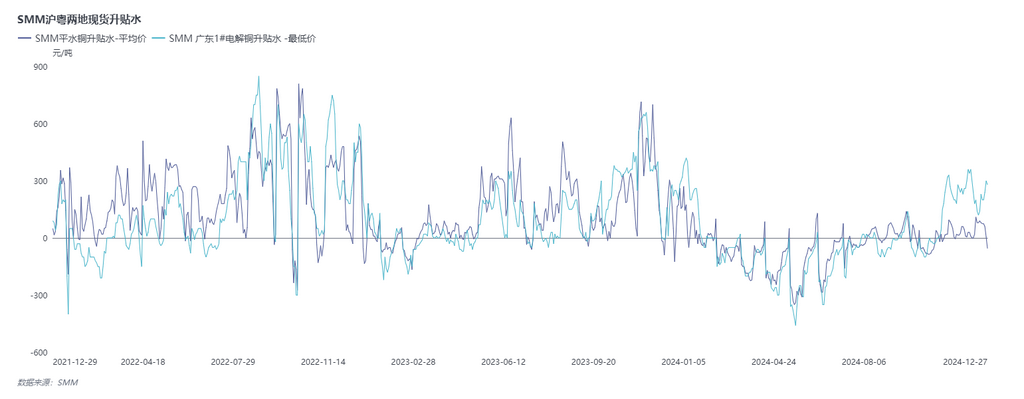

As the year-end approaches, most companies begin to settle accounts, and before this, smelters, traders, and others face inventory clearance targets. Year-end downstream purchase willingness decreases, forcing suppliers to adopt low-price clearance strategies. Within just two days, SHFE spot copper dropped by over 100 yuan per mt, and smelters in Shandong offered more competitive prices. Some downstream buyers in Jiangsu, Zhejiang, and Anhui preferred sourcing from this region, further suppressing prices in Shanghai.

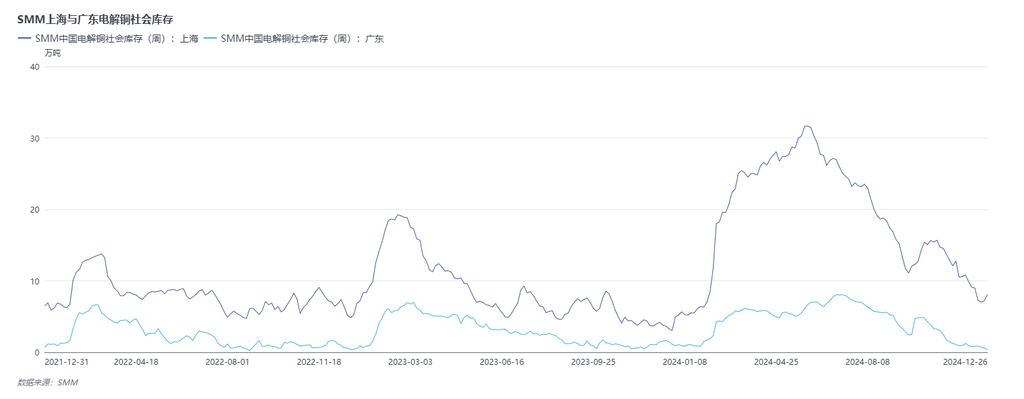

In contrast, spot premiums in Guangdong remained firm and climbed steadily at the year-end, mainly due to consecutive inventory declines. According to SMM data, as of December 26, Guangdong's inventory was only 3,800 mt, 5,200 mt lower YoY. Both imported and domestically produced arrivals in Guangdong were limited. While domestic arrivals in Shanghai were also scarce, sufficient imports provided a buffer, leading to further price suppression by downstream buyers.

Reviewing historical years, from 2022 to 2024, the Shanghai-Guangdong price spread consistently widened at the year-end. This was primarily due to Shanghai suppliers actively clearing inventory at low prices, while Guangdong's inventory remained extremely low, supporting spot premiums. However, due to the year-end timing, even with arbitrageable price spreads between the two regions, traders found it challenging to execute actual arbitrage.

It is expected that after the new year, the inventory clearance pressure on Shanghai suppliers will ease, and the Shanghai-Guangdong price spread will gradually narrow.

》View SMM Metal Industry Chain Database