》Check SMM Copper Quotes, Data, and Market Analysis

》Subscribe to View SMM Historical Spot Metal Prices

》Click to Access the SMM Copper Industry Chain Database

SMM, December 20:

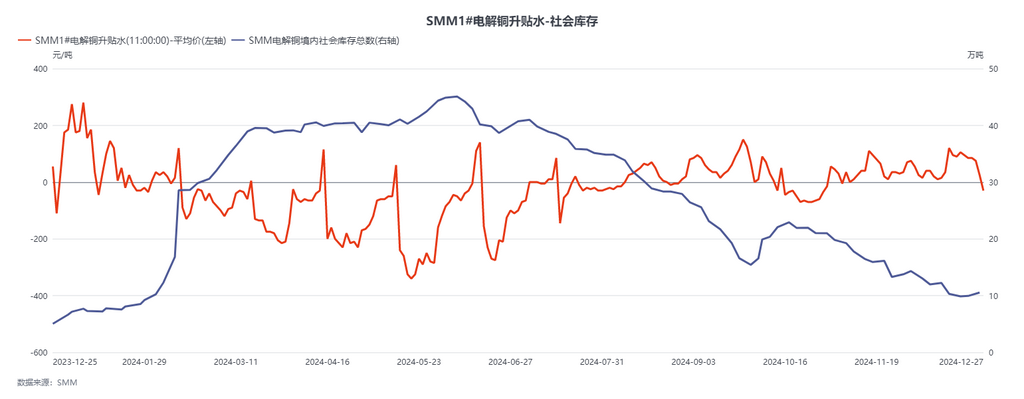

This week, SHFE copper spot premiums significantly declined, shifting from premiums to discounts. What are the reasons behind this sharp decline near the year-end? Below is a detailed analysis.

From the perspective of reasons, this week's decline in premiums is not closely related to changes in social inventory. The key lies in the supply-demand imbalance at various ports before the year-end. Specifically, the reasons can be summarized as follows: 1. Year-end closing by traders and the shift in business focus to payment collection after the execution of long-term contracts. Typically, by mid-to-late December, many traders have completed their long-term contract businesses, especially those based on annual contracts or long-term agreements. As their business focus shifts to payment collection, traders reduce their involvement in the spot market and concentrate more on clearing and recovering payments. Consequently, buying demand in the spot market decreases relatively. 2. Downstream processing enterprises have a high demand for cargoes with invoices dated this month, with fewer cross-year account executions, leading to more purchases directly from smelters, and the actual transaction center is relatively higher. Since smelters provide more stable supplies and can directly meet the demand for invoices dated this month, with fewer cross-year account executions, enterprises' purchasing demand is concentrated, resulting in the actual transaction center leaning towards smelters. 3. Concentrated and large arrivals of imported copper in Shanghai, creating a short-term oversupply. Due to the SHFE/LME price ratio remaining wide open for three consecutive weeks, the arrivals of imported copper in Shanghai have significantly increased, leading to a notable easing on the supply side. The lower import costs have allowed some imported copper offers to have greater room for price reductions, further suppressing spot market premiums.

Looking ahead, starting in 2025, the possibility of a rebound in copper spot market premiums and discounts is relatively high. Given the current low market inventory, low smelter inventory, and the potential for traders to resume restocking in anticipation of demand recovery, these factors combined are expected to push premiums higher as traders rebuild inventories at the beginning of the new year. As the supply-demand tension intensifies, the restocking demand from traders and smelters is expected to further lift spot prices, with the center of spot premiums likely to gradually rise.