》View SMM Copper Quotes, Data, and Market Analysis

》Click to View Historical Price Trends of SMM Spot Copper

Supply of Secondary Copper Raw Material Remains Tight

Entering December, the secondary copper raw material market remained deeply mired in a supply deficit, with no significant signs of relief. In overseas markets, as many countries entered holiday mode, market activity dropped sharply, and the overall number of offers was scarce, further exacerbating the shortage of secondary copper raw materials. Meanwhile, according to feedback from Ningbo import traders, due to year-end capital recovery needs and weak downstream purchase willingness, overall procurement volume continued to decline. Although a small amount of cargo has recently arrived at ports, most of these shipments were pre-booked, thus failing to alleviate the spot supply in the market.

Under Policy Influence, Secondary Copper Rod Enterprises Adopt a Wait-and-See Attitude

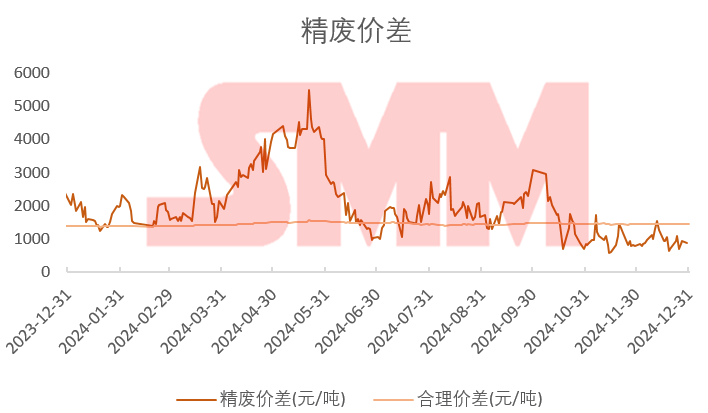

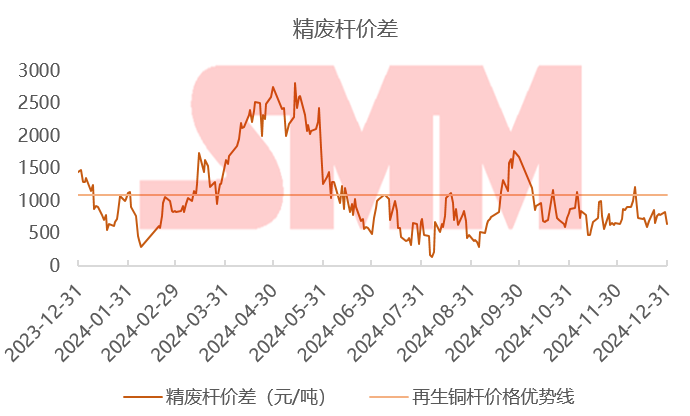

As of December 31, the price difference between primary metal and scrap for copper rods was 650 yuan/mt, significantly lower than the level of over 1,000 yuan/mt in mid-December, showing a narrowing trend overall, which has eroded the economic benefits of secondary copper rod enterprises. Additionally, facing the "reverse invoicing" policy set to be implemented in January 2025, downstream secondary copper rod plants generally adopted a cautious stance.

Some secondary copper rod plants have recently been actively stockpiling in hopes of maintaining production stability after the policy takes effect. Meanwhile, some secondary copper rod plants have started to suppress prices for secondary copper raw materials to mitigate cost risks, prompting suppliers to offload goods to avoid potential losses.

This series of chain reactions has slightly improved the supply situation in the domestic secondary copper raw material market in recent days. However, overall, the supply tension has not been fundamentally resolved. Nevertheless, this price suppression behavior may lead to an expansion trend in the price difference between primary metal and scrap at year-end.