SMM, December 31:

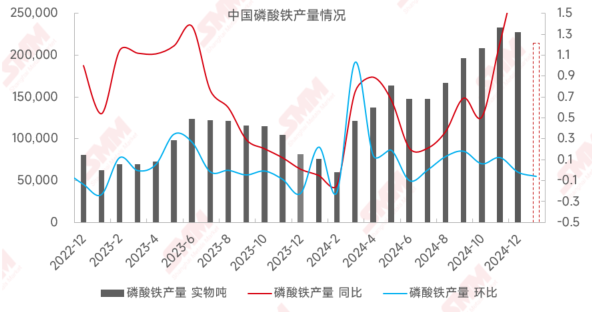

In December, China's iron phosphate production decreased 2% MoM, up 185% YoY.

Supply side in December, iron phosphate enterprises maintained a high operating rate to ensure sufficient raw material supply for downstream LFP production. Some iron phosphate enterprises had full order books, leading to a significant increase in production.

Raw material side, the prices of phosphoric acid and industrial monoammonium phosphate remained high. Additionally, due to production cuts caused by weak demand for titanium dioxide, the supply of ferrous sulphate, a by-product, also declined. The iron phosphate market showed strong demand for ferrous sulphate, driving its price upward throughout December. Consequently, the costs of iron phosphate produced via ammonium and sodium methods increased. Coupled with changes in the supply-demand relationship, iron phosphate enterprises stood firm on quotes, resulting in a price increase for iron phosphate in late December.

As late December marked both the month-end and year-end, it was a critical period for negotiating orders. Iron phosphate enterprises suffering prolonged losses had a strong desire to raise prices to mitigate losses.

In January, most iron phosphate enterprises are expected to have sufficient orders and maintain normal production during the Chinese New Year. Some enterprises plan to conduct maintenance and production line upgrades before the holiday, which may impact January's production. Iron phosphate production in January is expected to decline 6% MoM, up 183% YoY.

SMM New Energy Research Team

Cong Wang 021-51666838

Rui Ma 021-51595780

Ying Xu 021-51666707

Disheng Feng 021-51666714

Yujun Liu 021-20707895

Yanlin Lü 021-20707875