SMM January 2 News:

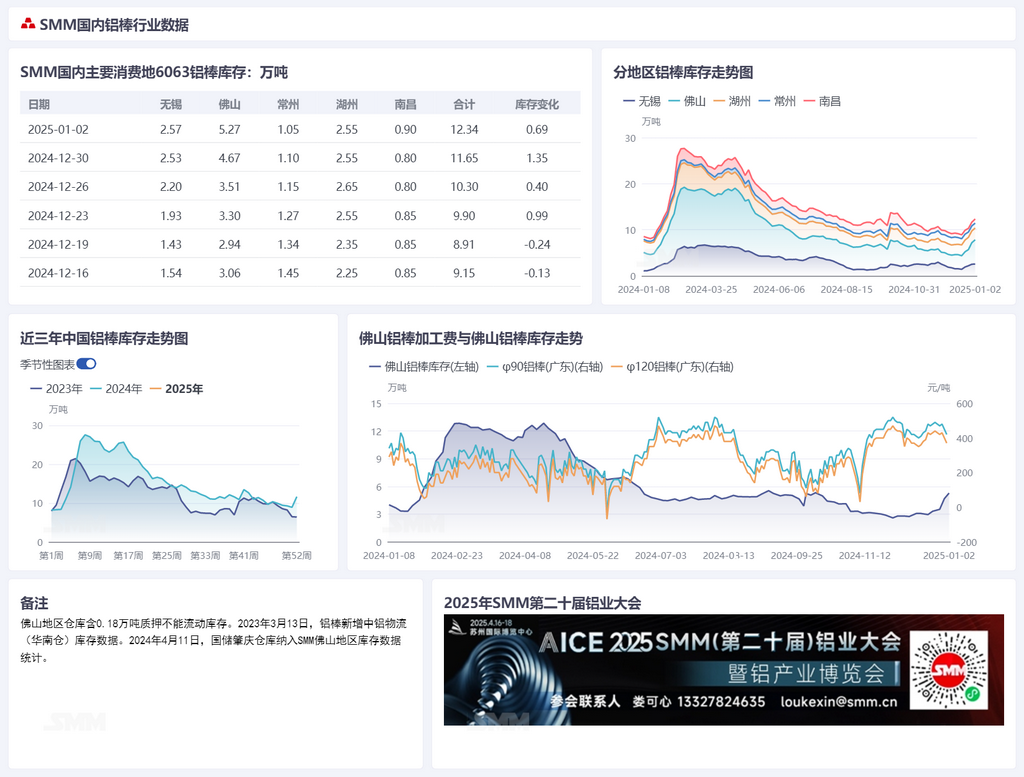

Regarding aluminum billet inventory, with the initial turning point in aluminum billet inventory and outflows from warehouses observed last week, this week the turning point has been further consolidated, aligning with downstream consumption expectations. In terms of aluminum billet inventory, due to the continuous increase in in-transit shipments from north-west China, including Xinjiang and Ningxia, concentrated arrivals occurred over the weekend. According to SMM statistics, as of January 2, 2025, domestic aluminum billet social inventory stood at 123,400 mt, marking a significant inventory buildup of 20,400 mt WoW. Following consecutive large inventory buildups, domestic aluminum billet supply has become relatively ample. On a YoY basis, the gap compared to the same period last year widened further to 41,400 mt, remaining at a three-year high for the same period. Among these, the South China region saw an inventory buildup of over 10,000 mt over the weekend. According to the SMM survey, current aluminum billet inventory in South China is mainly sourced from Guangxi, Yunnan, and recently increased supplies from Ningxia and Qinghai, while Xinjiang supplies remain in transit and have not yet arrived. Regarding outflows from warehouses, last week aluminum billet outflows increased slightly by 2,400 mt WoW to 41,700 mt, showing relatively stable performance.

In terms of processing fees, aluminum prices fluctuated rangebound this week, while year-end downstream demand for aluminum processing remained weak, putting downward pressure on aluminum billet processing fees. According to the SMM survey, aluminum billet manufacturers, facing pessimistic expectations at year-end, have implemented production cuts to alleviate inventory pressure and ensure a smooth transition. Consequently, operating capacity on the supply side has declined. However, operating rates of downstream profile manufacturers have not shown optimistic performance, and with the upcoming holiday period at the end of January, rigid demand for raw material procurement has significantly decreased. Supply remains relatively ample, and market transactions are weak. By region, Foshan saw stable aluminum billet shipments this week, but recent arrivals have been substantial, accelerating warehouse inventory growth. The processing fee for φ120 aluminum billets was 330 yuan/mt, down 90 yuan/mt WoW. In Wuxi, the off-season atmosphere prevailed, with market transactions progressing steadily. The processing fee for φ120 aluminum billets remained unchanged at 380 yuan/mt WoW. In Nanchang, market supply was tight, and downstream purchasing was weak, putting pressure on processing fees. The processing fee for φ120 aluminum billets was 400 yuan/mt, down 50 yuan/mt WoW.

》Subscribe to View SMM Historical Spot Metal Prices

》Click to Access the SMM Aluminum Industry Chain Database