SMM, January 3:

Reviewing 2024, the copper anode market experienced multiple turning points amid significant fluctuations in copper concentrates and secondary copper raw materials.

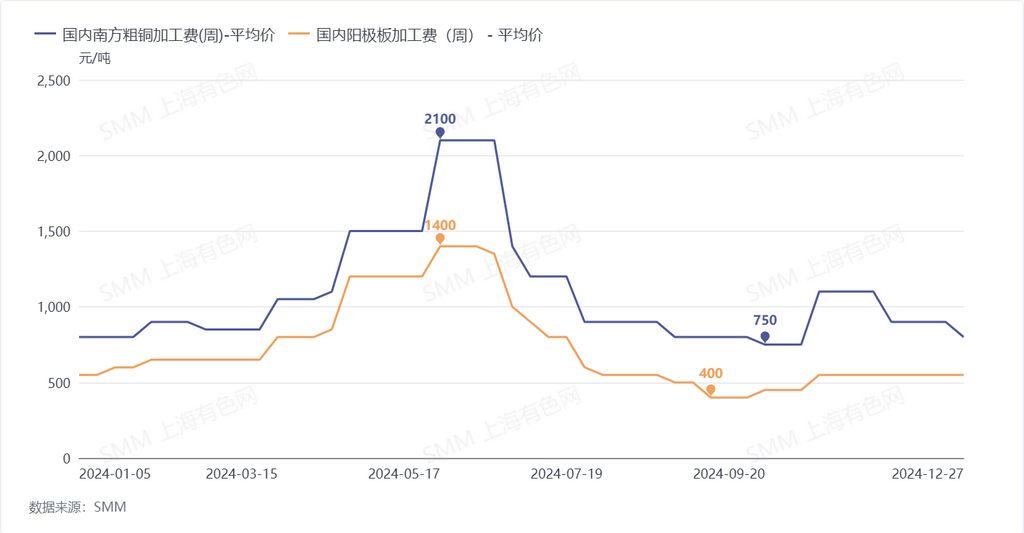

At the beginning of the year, the suspension or production cuts at several copper mines reversed market expectations for mine-side balance. The spot TC for copper concentrates plummeted, leading to significant losses for smelters using spot copper concentrates for production. This forced smelters to actively seek alternative raw materials, driving up demand for copper anodes. Meanwhile, some copper anode smelters suspended production due to losses.

The first turning point of the year occurred in Q2. As copper prices surged to record highs, secondary copper suppliers began offloading large inventories, rapidly widening the price difference between primary metal and scrap. The surge in secondary copper raw material supply led to a sharp increase in domestic copper anode production. However, downstream consumption was suppressed by high copper prices, weakening overall demand for secondary copper rods. This resulted in significantly higher profits for copper anodes compared to secondary copper rods. Many secondary copper rod plants switched to producing copper anodes or installed rotary casting equipment. Domestic supply temporarily exceeded demand, pushing blister copper spot RC to a multi-year high of over 2,000 yuan/mt, with significant volumes from south China being shipped to the north.

Entering Q3, the market saw a second turning point. As copper prices fell back from highs, the supply of secondary copper raw materials declined rapidly. Following this, the implementation of the Fair Competition Review Regulations on August 1 led to widespread production cuts and shutdowns among scrap utilisation enterprises. The supply-demand structure for copper anodes reversed sharply, and processing fees plunged to the bottom. Subsequently, concerns over tariff policies under Trump's administration reduced copper scrap imports, and the impending implementation of the "directional invoicing" policy further tightened the copper anode market.

Moving into 2025, the copper anode market remains under close watch. The foreseeable shortage of copper concentrates, with the TC long-term contract benchmark at only $21.25/mt, forces smelters to face losses directly. With limited imported copper anode supply, the domestic market is expected to remain highly active.