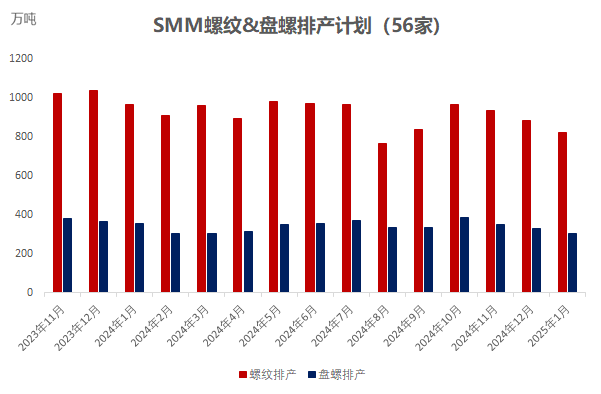

Since April 2022, the SMM rebar production schedule sample has been expanded to 56 enterprises.

According to SMM survey data from 56 key steel producers:

- The planned rebar production for January is 8.2143 million mt, down 613,500 mt from the actual production in December, a decrease of 6.95%.

- The planned wire rod production for January is 3.0585 million mt, down 299,900 mt from the actual production in December, a decrease of 8.93%.

Chart-1: Production Schedule of Rebar & Coiled Rebar by Major Construction Steel Mills (56 Enterprises)

Source: SMM

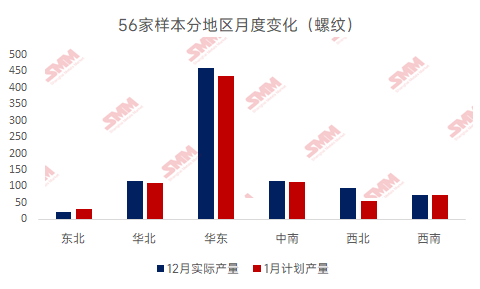

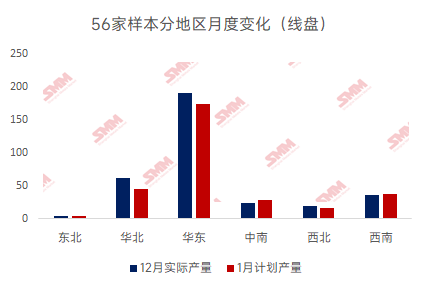

By region (56 enterprises):

North-East China: The planned rebar production totals 307,300 mt, up 98,000 mt MoM, an increase of 46.82%. The planned wire rod production totals 40,000 mt, up 5,000 mt MoM, an increase of 14.29%. ;

North China: The planned rebar production totals 1.098 million mt, down 68,000 mt MoM, a decrease of 5.83%. The planned wire rod production totals 448,000 mt, down 178,000 mt MoM, a decrease of 28.43%.

East China: The planned rebar production totals 4.364 million mt, down 229,500 mt MoM, a decrease of 5%. The planned wire rod production totals 1.7455 million mt, down 166,900 mt MoM, a decrease of 8.73%.

Central-South China: The planned rebar production totals 1.171 million mt, down 41,000 mt MoM, a decrease of 3.5%. The planned wire rod production totals 283,000 mt, up 46,000 mt MoM, an increase of 19.41%.

North-West China: The planned rebar production totals 565,000 mt, down 385,000 mt MoM, a decrease of 40.53%. The planned wire rod production totals 165,000 mt, down 29,000 mt MoM, a decrease of 14.95%.

South-West China: The planned rebar production totals 750,000 mt, up 12,000 mt MoM, an increase of 1.63%. The planned wire rod production totals 377,000 mt, up 23,000 mt MoM, an increase of 6.5%.

Chart-2: Monthly Regional Changes in Rebar Production

Source: SMM

Chart-3: Monthly Regional Changes in Wire Rod Production

Source: SMM

Overall:

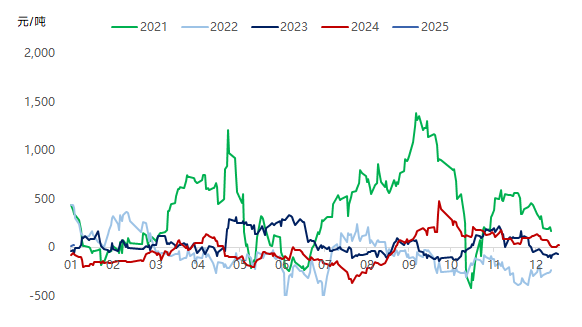

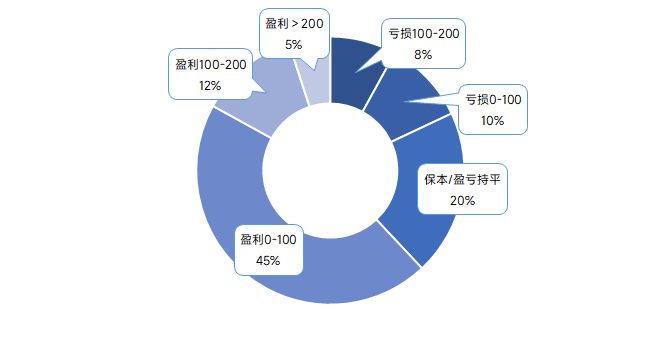

In December, construction steel prices fluctuated rangebound with reduced frequency of price changes. The market sentiment was a mix of strong expectations for the economic conference and weak winter stockpiling sentiment. Meanwhile, downstream demand gradually weakened, and overall market trading activity declined. On the cost side, iron ore prices adjusted slightly, coke fundamentals remained weak, and the profitability of construction steel production at steel mills varied. Except for widespread losses in north-west China, other regions saw moderate profits, ranging from (-200, 200). Considering profitability factors, steel mills in north China postponed their year-end breaks to January, while some areas in east China implemented production controls, and other regions increased maintenance. On the electric furnace side, with the Chinese New Year approaching, most electric furnace mills have finalized their winter break plans, and the operating rate is expected to drop to a low point in late January. The planned production of rebar and coiled rebar in January continues to decline.

By region:

North-East China: Steel mill profits ranged from (0-100). At the end of December, some steel mills in the region resumed production. Although steel billets were still sold externally, the increase in pig iron production led to higher construction steel output in January, mainly in rebar.

North China: Steel mill profits ranged from (0-200). Maintenance plans for steel mills in the region at the end of 2024 were postponed to January, resulting in a decline in construction steel production in January. .

East China: Steel mill profits ranged from (100-200). Some steel mills in the region resumed production, while others implemented production controls. The increase in production from resumption was smaller than the reduction from controls, leading to an overall decrease in construction steel production schedules in January.

North-West China: Steel mill profits ranged from (-200-(-100)). Steel mills in north-west China faced high production costs and poor profitability. Additional blast furnace and rolling line maintenance in January led to a significant decline in construction steel production plans.

Central-South China: Steel mill profits ranged from (-50-100). Maintenance from earlier periods continued in the region, with some mills completing maintenance and resuming production in late January. Rebar production decreased while wire rod production increased, resulting in little overall change in construction steel output.

South-West China , Steel mill profits ranged from (-50-100). The steady ramp-up of production following the commissioning of new blast furnaces led to a slight increase in construction steel production schedules in January.

Chart-4: Real-Time Profit Trends of Rebar Production by Steel Mills Since 2020

Source: SMM

Chart-5: Marginal Profitability of Rebar at Sample Steel Mills in Early October

Source: SMM

Looking ahead:

At month-end, coinciding with the Chinese New Year, most steel mills in north China will officially begin year-end maintenance. Additional maintenance will also occur in north-west, south-west, and central China. The daily planned rebar production schedule for January is expected to continue declining compared to December. Meanwhile, most electric furnace mills will begin their year-end breaks in mid-January, with resumption expected after the Chinese New Year. The operating rate of sample electric furnace mills is projected to drop to a low point in late January. On the demand side, outdoor construction conditions in south China remain moderate. However, with the Chinese New Year approaching and cold air moving in, terminal projects will gradually shut down starting mid-month as workers return home. Some rush-to-meet-deadline projects may continue until the holiday, but their demand will be limited, and overall terminal demand will gradually stagnate.

Additionally, January falls within a domestic macro vacuum period. Winter stockpiling policies from steel mills are being intensively introduced across regions. However, according to SMM surveys, market-driven winter stockpiling has significantly weakened compared to previous years. Some agents opted for interest-bearing payment without locking in goods, others passively converted regular volumes into winter stockpiles, and some market participants abandoned winter stockpiling altogether. Overall, construction steel supply will continue to decline in January, with the inventory turning point occurring later than in previous years. Low supply, low demand, and low inventory, coupled with low market activity, will limit fluctuations in spot prices. Prices are expected to stabilize after mid-month, with the market restarting after the Chinese New Year.