The 2024 Year-End "Performance Report" for Lithium Carbonate Is Here!

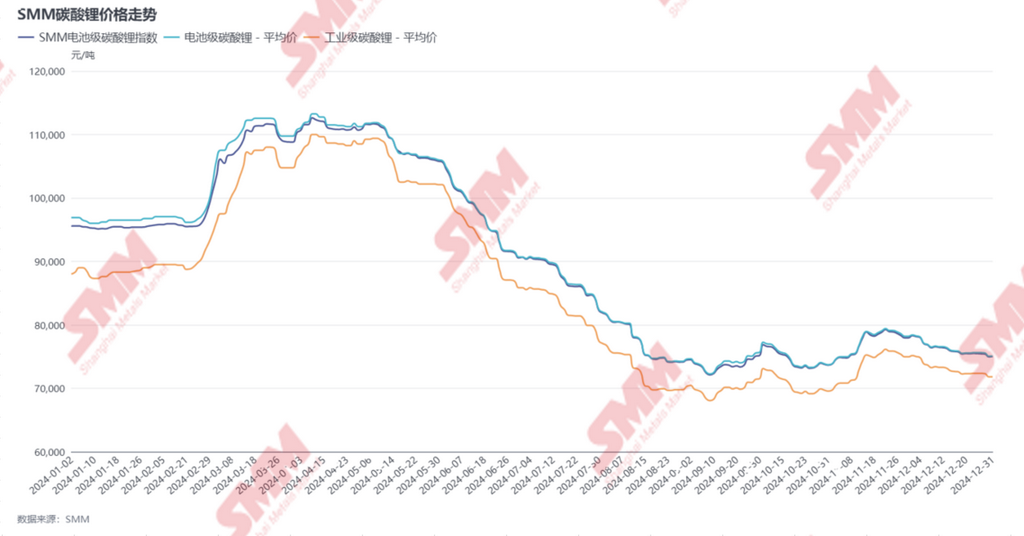

I. Price Review

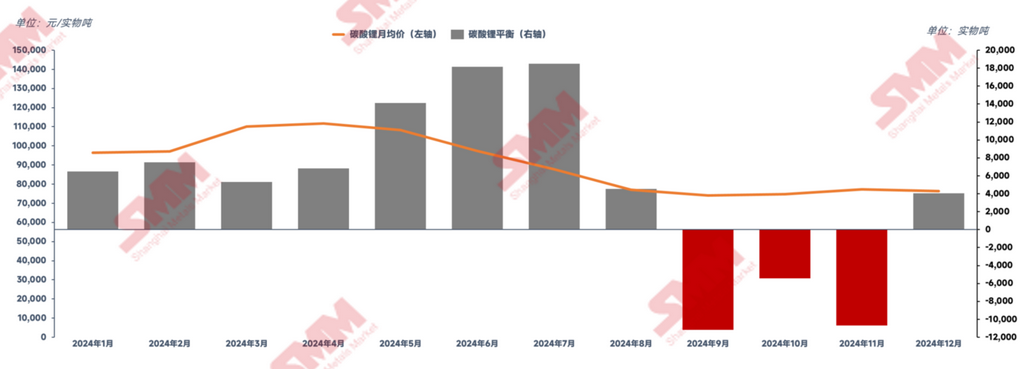

2024 was a highly volatile year for lithium carbonate prices. Although it was not as dramatic as the "free fall" from 500,000 yuan/mt to 100,000 yuan/mt in 2023, the prices in 2024 experienced a "roller coaster" ride due to cyclical supply-demand mismatches and occasional overseas export rushes. The highest price reached around 110,000 yuan/mt, the lowest dropped to 72,000 yuan/mt, and the annual average was 90,000 yuan/mt. Following the saying "after all the ups and downs, it still ends at 90,000," the annual average price in 2024 once again settled at 90,000 yuan/mt.

Phase-by-Phase Price Review:

January 2024 to Early February 2024

In the short term, futures prices were higher than spot prices, prompting some lithium chemical plants to transfer to delivery warehouses and strengthening their sentiment to stand firm on quotes. In late January, some cathode plants, considering the logistics suspension during the Chinese New Year, conducted limited pre-holiday restocking, slightly boosting lithium chemical prices. Late February 2024 to Early April 2024

Environmental protection checks in Jiangxi, combined with maintenance and production cuts at major lithium chemical plants in Sichuan, led to market expectations of

a short-term reduction in lithium chemical supply after the holiday. Coupled with the price war in the EV sector and the launch of new car models in March, which significantly boosted demand, lithium chemical spot prices rose. Meanwhile, some lithium chemical enterprises stood firm on quotes and were reluctant to sell, resulting in a scarcity of low-priced cargoes in the spot market and a steady price increase. Late April 2024 to Late August 2024

Upstream lithium chemical supply remained at high levels, but the slowing growth in NEV end-use demand led to reduced production schedules at cathode plants. Most cathode plants maintained high lithium chemical inventory levels in Q2, and

long-term contracts and customer-supplied volumes recovered significantly from May to July, focusing on just-in-time procurement for spot orders with no restocking plans. The lithium carbonate spot trading market was relatively quiet, and prices continued to decline. Early September 2024 to Late November 2024 In September, significant production cuts at major lithium chemical plants in Jiangxi led to a notable impact on downstream customer supply volumes. Combined with the continued increase in downstream production schedules

and widespread pre-holiday restocking for the National Day, spot procurement demand for lithium carbonate was significantly boosted,

slowing the decline in spot prices and causing a slight rebound. From late October, driven by the year-end rush for installations by end-users, both downstream material plants and upstream smelters increased production schedules, making lithium carbonate spot transactions relatively active and slightly lifting the transaction price center in October and November. Early December 2024 to Late December 2024 The price rebound stimulated upstream smelters' production enthusiasm, leading to a continuous increase in domestic lithium carbonate supply. However, during the period of negotiations for long-term contract discounts for 2025, upstream lithium chemical plants maintained a strong sentiment to stand firm on quotes for both long-term contracts and spot cargoes. From the December transaction data, downstream material plants had already started pre-holiday restocking, while traders, facing high inventory levels, aimed to destock and recover funds at year-end by promoting transactions with downstream material plants at relatively low price points.

The market was relatively active, and prices showed a slight decline.

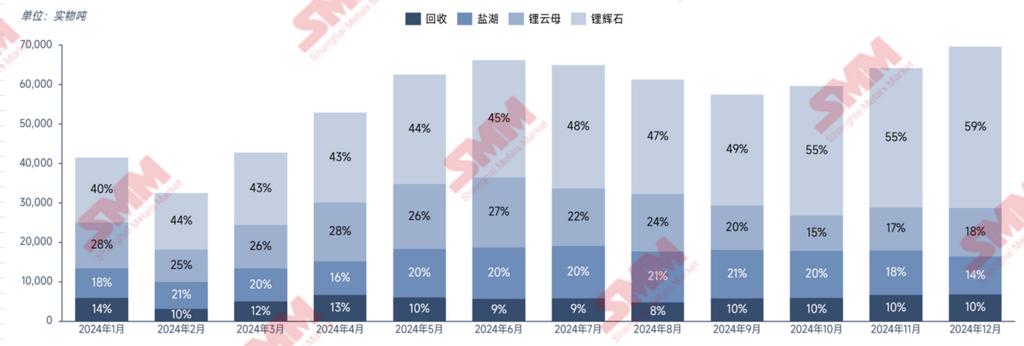

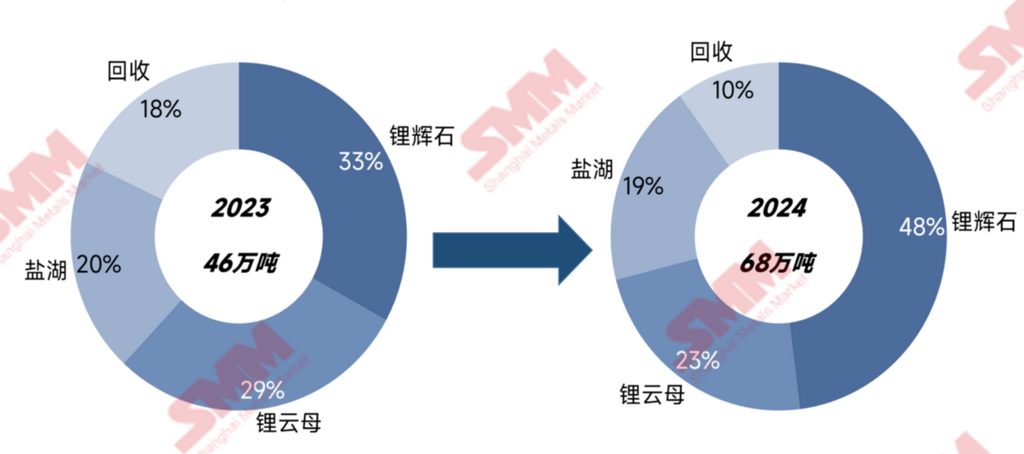

II. Supply-Side Review 1. Domestic Production In 2024, China's total lithium carbonate production reached approximately 680,000 mt, up 47% YoY. By raw material type: Spodumene accounted for nearly half

,

with a share of about 48%, up 116% YoY.

This was mainly driven by the commissioning of new production lines at integrated lithium chemical plants, as well as the relatively sluggish demand for lithium hydroxide, the continued expansion of the price spread between lithium carbonate and lithium hydroxide, and the shift of some lithium hydroxide production lines to supplement lithium carbonate output, significantly increasing spodumene-derived lithium carbonate production. Lepidolite, affected by high cost pressures and environmental protection issues, combined with tight supply of high-grade lepidolite in Jiangxi, saw a slower production growth rate, up 17% YoY. Salt lake production, benefiting from its cost advantages, continued to expand, up 37% YoY. Recycling, constrained by structural shortages of raw materials caused by regional mismatches in waste battery resources, faced inefficient capacity utilization. Combined with profit losses, production in 2024 declined by 19% YoY, accounting for only 10% of the total. 2. Overseas Imports According to customs data, China's lithium carbonate imports in 2024 amounted to approximately 230,000 mt, up 46% YoY. Chile and Argentina remained China's main import sources. Specifically: Imports from Chile totaled about 180,000 mt, up 29% YoY, accounting for 78% of China's total imports. Imports from Argentina totaled about 45,000 mt, up 156% YoY, accounting for 20% of China's total imports. On the export side, China's lithium carbonate export share remained small, and the overall overseas demand showed no significant improvement. With overseas salt lake lithium carbonate production costs being relatively more competitive, China's lithium carbonate exports in 2024 were less than 5,000 mt. III. Demand-Side Review

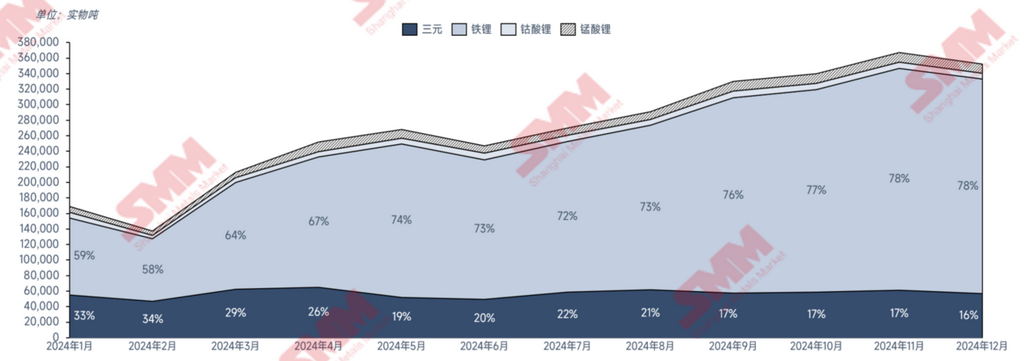

Driven by the rapid development of the NEV sector and the ESS market,

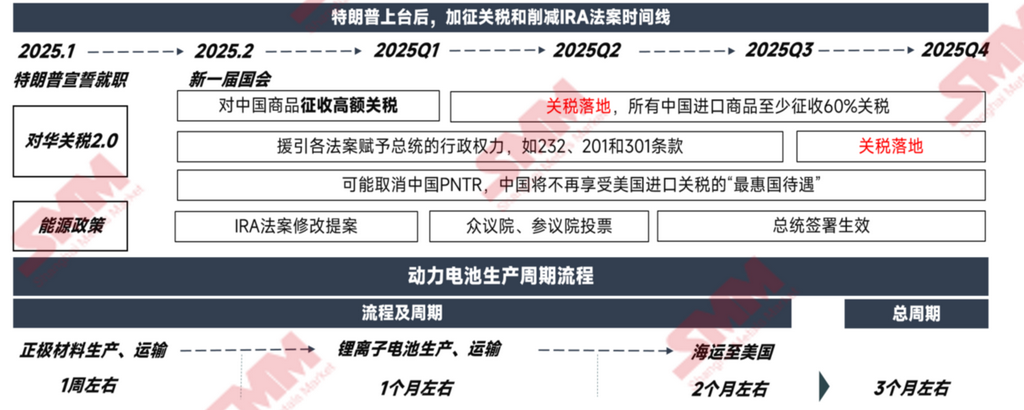

China's lithium carbonate demand in 2024 reached approximately 850,000 mt LCE, up 44% YoY. By application: 67% was used for LFP cathode material production, and 12% for ternary cathode material production. Ternary cathode materials not only saw a decline in market share but also a reduction in lithium carbonate consumption. On one hand, domestic NEVs increasingly favored LFP battery cells, while the ESS market continued to expand its share due to the high safety of LFP battery cells. On the other hand, the growing proportion of high-nickel content in ternary 6-series materials also reduced lithium carbonate consumption. On one hand, the policy uncertainty brought by the US presidential election results led domestic battery cell enterprises to rush for overseas exports in Q4 2024. On the other hand, the continuous strengthening of China's trade-in policy, along with the cumulative effects of policies and promotional activities by local governments and enterprises, drove car sales enthusiasm to remain high. With domestic and overseas demand both exceeding expectations, the post-September-October peak season saw an even more remarkable November-December, with demand reaching its annual peak. However, the rush effect driven by the US election only advanced future demand. While the recent surge was strong, it may have overdrawn future demand, leading to a potential decline in overseas export volumes.

IV. Supply-Demand Balance

In 2024, lithium carbonate continued to experience an inventory buildup,

with an annual surplus of approximately 60,000 mt and cumulative inventory of about 110,000 mt (sample statistics). On one hand, significant production cuts at a major lithium chemical plant in Jiangxi in early September led to a noticeable reduction in lithium carbonate supply. On the other hand, the peak season effect driven by demand exceeding expectations from September to November resulted in a destocking trend. Overall, the supply surplus persisted. V. 2025 Outlook Demand side, China remains the leading country for NEVs and ESS. In the power market, the Central Political Bureau's meeting on December 9 indicated that the policy environment in 2025 would remain favorable for the healthy development of the automotive industry. Additionally, as 2025 marks the final year of the 14th Five-Year Plan, consumer demand for car replacements is expected to surge. SMM holds an optimistic outlook for car sales in 2025, forecasting an annual growth rate of over 20%. In the ESS market, driven by policies, China's performance in 2025 is expected to remain strong, with a growth rate also projected to exceed 20%.

Supply side, the current overall operating rate of upstream lithium chemical plants is only 50%-60%. With some new capacity still awaiting commissioning in 2025, domestic lithium carbonate production is expected to grow by over 25%. In the future, the industry's degree of integration will deepen. With the continuous release of overseas lithium carbonate capacity and the relatively slow growth in overseas demand, the surplus of overseas lithium carbonate will intensify, promoting more low-cost lithium carbonate to flow into the Chinese market. This will pose certain resistance to the growth of high-cost lithium chemical plants, potentially leading to reductions or even exits.

In 2025, both supply and demand for lithium carbonate are expected to increase, but supply growth will outpace demand, further expanding the annual surplus.

Lithium carbonate prices are expected to face some downside room. Although current prices are already approaching the cost line for some lithium mines, the strong sentiment among lithium miners to stand firm on quotes may provide some support for lithium carbonate production costs.

However, with the deepening of low-cost integration in the industry and the continuous increase in imports, the price center of domestic lithium carbonate still has room to decline. The industry's hope for lithium carbonate to return to 100,000 yuan/mt may remain a distant dream.

SMM New Energy Industry Research Department

Cong Wang 021-51666838 Xiaodan Yu 021-20707870 Rui Ma 021-51595780 Ying Xu 021-51666707 Disheng Feng 021-51666714

Yujun Liu 021-20707895 Yanlin Lü 021-20707875 Zhicheng Zhou 021-51666711 Haohan Zhang 021-51666752

Zihan Wang 021-51666914 Xiaoxuan Ren 021-20707866 Yushuo Liang 021-20707892 Jie Wang 021-51595902

Yang Xu 021-51666760