In 2024, cobalt sulphate prices primarily trended downward, hitting new lows throughout the year. The term "nickel-cobalt price parity" also became a label for cobalt sulphate in 2024.

I. Price Overview:

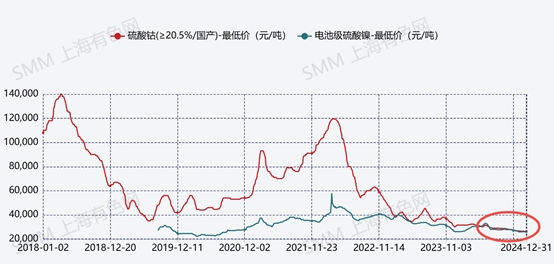

According to the SMM website, the average of low-end prices for cobalt sulphate in 2024 was 29,500 yuan/mt, down 22% YoY compared to the same period in 2023. The lowest low-end price during the year was 26,300 yuan/mt.

From a quarterly price review perspective:

Q1 2024: Supply side, due to high raw material prices and elevated costs, cobalt salt production fell short of expectations. However, with high inventory levels in the social circulation chain, overall supply remained sufficient. Demand side, procurement of precursors and Co3O4 was substantial in earlier periods, leading to limited new purchase willingness. Most demand was self-supplied, resulting in muted demand for circulating materials. Overall, high inventory levels in the trading chain led some traders to offload small quantities of cobalt salts at the end of the quarter due to cash flow pressures, driving prices downward.

Q2 2024: Downstream ternary cathode precursor production schedules declined, and demand for Co3O4 also weakened, reducing cobalt demand. Supply side, although cobalt salt producers reduced output due to cost and sales pressures, accumulated inventories from earlier periods prevented a shift in the supply-demand pattern. Price reductions to stimulate transactions further dragged down cobalt sulphate spot prices.

Q3 2024: Supply side, limited spot purchases due to low market activity led cobalt sulphate smelters to maintain production cuts and destocking. Demand side, downstream ternary cathode precursor and Co3O4 markets showed weak willingness for spot raw material purchases, with a high proportion of customer-supplied or self-supplied materials. The oversupply situation persisted, and spot prices continued to decline.

Q4 2024: Downstream ternary cathode precursor production schedules declined, reducing cobalt sulphate demand. Supply side, cobalt sulphate smelters maintained low operating rates, focusing on destocking. In early November, significant low-priced sales in the market temporarily pushed spot prices down, followed by a brief rebound after destocking reached a certain level. However, as market confidence in cobalt waned, the willingness to stand firm on quotes weakened. Combined with limited spot purchase demand, cobalt sulphate spot prices continued to decline.

II. Supply Overview:

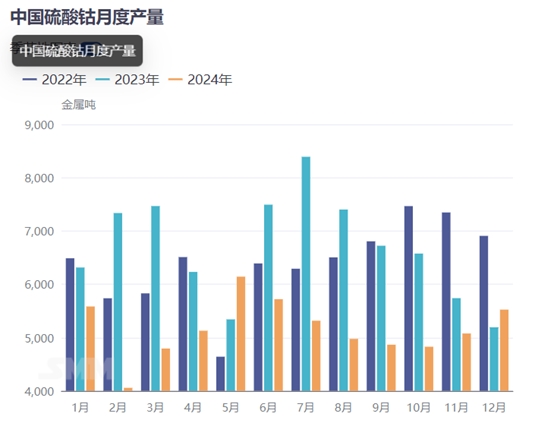

According to SMM, China's total cobalt sulphate production in 2024 was approximately 62,000 mt in metal content (excluding cobalt sulphate production from refined cobalt integration), down 24% YoY compared to 2023. Recycled materials accounted for only 14% of the output. The significant production decline was primarily due to two factors: first, cobalt salt overcapacity and high integration demand concentration in the market increased pressure on smelters solely producing cobalt sulphate. Second, prolonged sluggish sales resulted in high in-plant and social inventory levels. To reduce losses, cobalt sulphate smelters adopted production cuts and destocking measures, leading to a decline in overall production.

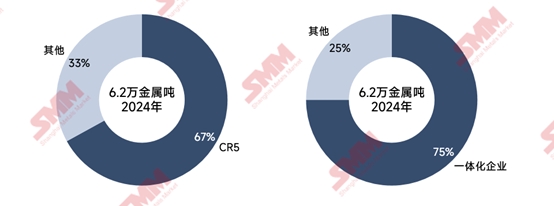

From the current market CR5 perspective, cobalt sulphate enterprises exhibit relatively high concentration, with a high degree of integration.

III. Demand Overview:

Cobalt sulphate's downstream demand is primarily in the ternary cathode precursor sector. In 2024, the continued market share erosion of ternary battery cells by LFP battery cells reduced cobalt sulphate consumption in the ternary cathode precursor sector. Additionally, although the consumer market grew rapidly in 2024, cobalt sulphate consumption in the Co3O4 sector remained limited. Most new Co3O4 capacity this year was concentrated in the cobalt chloride system, further restricting cobalt sulphate consumption.

IV. Supply and Demand Overview:

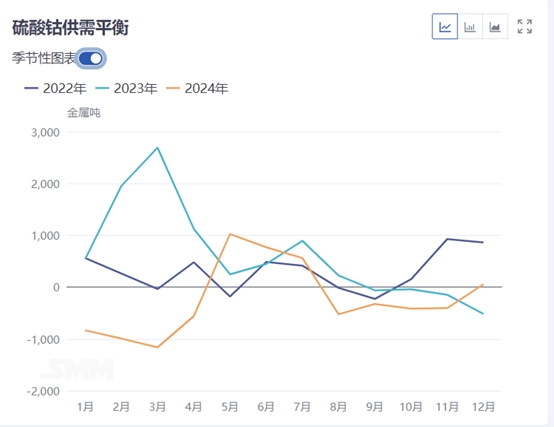

In 2024, downstream ternary cathode precursor demand focused on medium- and high-nickel directions, reducing cobalt sulphate demand. Moreover, demand in 2024 was concentrated among top-tier enterprises, intensifying the integrated market structure. Supply side, significant stockpiling by traders in 2023 extended into 2024, ensuring ample supply despite declining cobalt sulphate production. The market primarily focused on destocking throughout the year.

V. Outlook for 2025:

Demand side, with declining lithium prices, LFP battery cell cost advantages in the power sector may weaken, leaving room for NEV development. Additionally, the consumer market may benefit from the expansion of high-end electronic devices such as wearable devices and smart home equipment, supporting cobalt sulphate demand in the Co3O4 sector.

Supply side, with raw material oversupply and cobalt sulphate enterprises facing inventory pressures, production schedules may become more flexible, adjusting output based on demand.

Spot price outlook, declining raw material prices may weaken long-term cost support. As cobalt sulphate smelters adjust production based on demand, post-destocking, spot prices are expected to fluctuate within a reasonable profit range.

SMM New Energy Research Team

Cong Wang 021-51666838

Rui Ma 021-51595780

Disheng Feng 021-51666714

Ying Xu 021-51666707

Yanlin Lü 021-20707875

Yujun Liu 021-20707895

Xiaodan Yu 021-20707870

Zhicheng Zhou 021-51666711