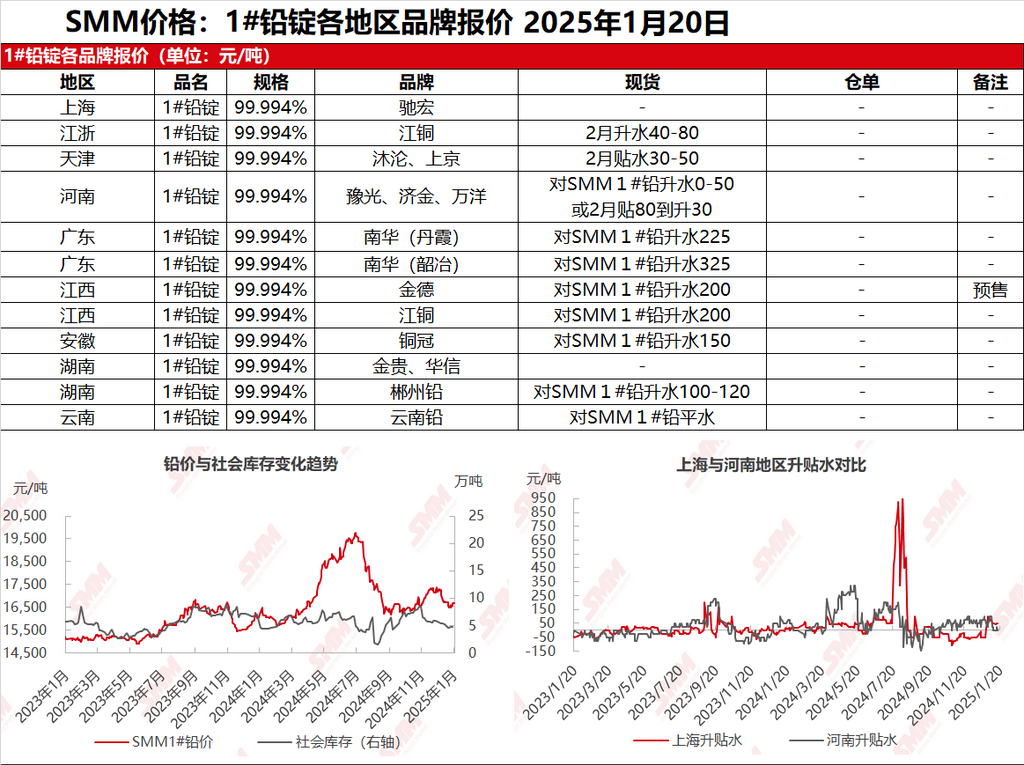

SMM, January 20: Quotations in the Shanghai market were scarce; JCC lead in Jiangsu and Zhejiang regions was quoted at 16,745-16,805 yuan/mt, with premiums of 40-80 yuan/mt against the SHFE 2502 contract. SHFE lead fluctuated upward, and suppliers had limited cargoes, with quotations significantly reduced WoW. During this period, some primary lead cargoes self-picked up from production sites were quoted in line with market trends, with premiums adjusted downward. Some secondary lead enterprises followed downstream to take holidays, resulting in reduced secondary refined lead quotations. Mainstream regions quoted secondary refined lead at premiums of 0-50 yuan/mt against the SMM 1# lead average price on an ex-factory basis. Downstream enterprises had either taken holidays or completed pre-holiday stockpiling, leading to sparse inquiries and sluggish spot order transactions.

Other markets: Today, the SMM 1# lead price remained flat compared to the previous trading day. In Henan, long-term contract cargo pick-up remained dominant, with some suppliers quoting discounts of 70-80 yuan/mt against the SHFE 2402 contract, and transactions were based on rigid downstream demand. In Hunan, premiums were adjusted downward to 100-120 yuan/mt, with weakened transactions. Meanwhile, in Jiangxi, Yunnan, Guangdong, and other regions, primary lead supply slightly recovered, and downstream pre-holiday stockpiling for rigid demand gradually ended, leading to weakening transactions.