During the Chinese New Year holiday, the total inventory of construction steel increased significantly, but overall inventory remained relatively low YoY. Specifically, rebar inventory rose 47.62% MoM from pre-holiday levels, while wire rod inventory increased 58.4% MoM. During the holiday, steel markets across the country were closed, downstream end-users halted construction activities, and overall demand stagnated. Spot prices remained stable, while total inventory accumulated rapidly, supported by lower steel mill production and an inventory turning point that occurred over a month later than in previous years. Post-holiday, overall inventory decreased significantly compared to the same period in previous lunar years. Currently, market traders are gradually returning, while downstream end-use demand is expected to recover progressively after the Lantern Festival. Inventory is expected to continue increasing next week.

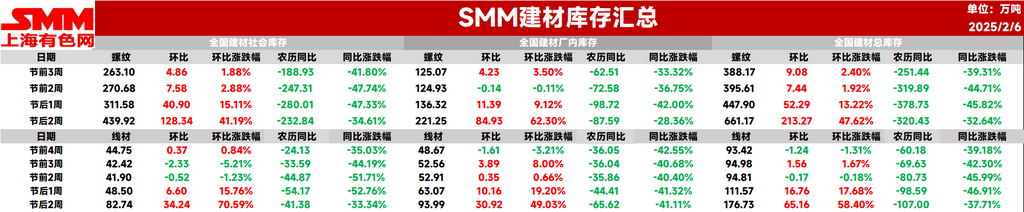

This week, total rebar inventory reached 6.6117 million mt, up 2.1327 million mt or 47.62% MoM from pre-holiday levels (previous value +13.22%), but down 3.2043 million mt or 32.64% YoY from the same period last lunar year (previous value -45.82%).

Table 1: Overview of Rebar Inventory

Source: SMM

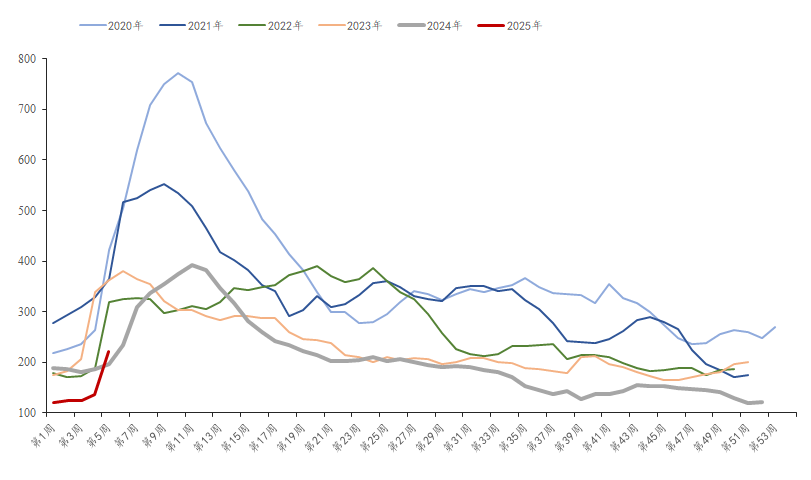

This week, in-plant rebar inventory stood at 2.2125 million mt, up 849,300 mt or 62.3% MoM from pre-holiday levels (previous value +9.12%), but down 875,900 mt or 28.36% YoY from the same period last lunar year (previous value -42%). During the Chinese New Year holiday, blast furnace steel mills, except for some blast furnaces undergoing annual maintenance, maintained normal production, leading to a rapid accumulation of in-plant inventory.

Chart-1: Rebar In-Plant Inventory Trends, 2019-2024

Source: SMM

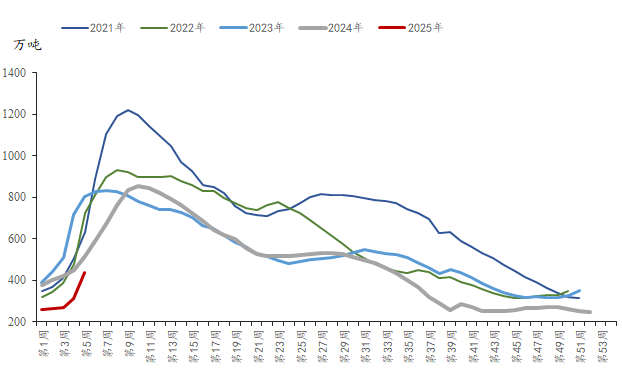

This week, social rebar inventory reached 4.3992 million mt, up 1.2834 million mt or 41.19% MoM from pre-holiday levels (previous value +15.11%), but down 2.3284 million mt or 34.61% YoY from the same period last year (previous value -47.33%). During the holiday, the market was largely closed, and with normal steel mill deliveries, social inventory increased significantly.

Chart-2: Rebar Social Inventory Trends, 2019-2024

Source: SMM

Looking ahead, according to the SMM survey, as the market gradually resumes operations, annual maintenance at some blast furnace steel mills is nearing completion, and most steel mills are operating with moderate profitability. There is some expectation for steel mills to resume production, with EAF steel mills expected to gradually restart production from the tenth day of the lunar calendar. Overall supply is expected to increase subsequently. Regarding demand, according to the SMM survey, most downstream end-use construction activities are expected to gradually resume on February 7, with full recovery likely by the end of February. Currently, the market is in a state of low production, low inventory, and low demand, which provides some support for spot prices. The pace of demand recovery will dominate spot price trends, while short-term market sentiment will primarily drive the market, leading to rangebound price fluctuations and continued inventory accumulation.