Weekly Review

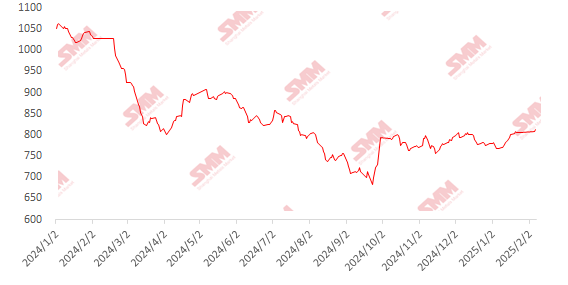

This week, imported iron ore prices first weakened and then strengthened. Macro side, during the Chinese New Year holiday, Trump signed an executive order imposing a 10% tariff on Chinese exports to the US and a 25% tariff on imports from Canada and Mexico. However, its instability caused market sentiment to fluctuate. As a result, iron ore futures prices on the first trading day after the holiday rose initially but then fell, showing significant volatility. Fundamentals side, domestic steel mills gradually resumed blast furnace operations, leading to a slight rebound in pig iron production. Coupled with the release of restocking demand from steel mills after the holiday, overall demand for iron ore increased. Although global iron ore shipments recovered, domestic rain and snow weather and the holiday affected work efficiency, leading to a slight decline in port arrivals and easing supply pressure. Supported by fundamentals, iron ore prices fluctuated upward. At the port, PB fines prices in Shandong rose by 15 yuan/mt WoW.

Chart: SMM62% Imported Ore MMi Index

Data Source: SMM

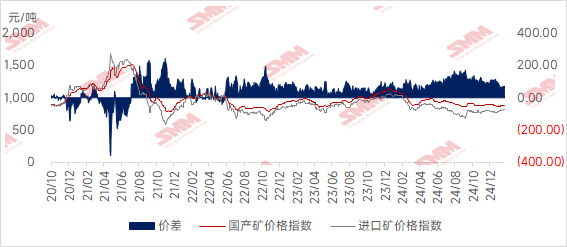

Domestic ore prices rose slightly after the holiday, and domestic ore prices are expected to continue climbing next week. This week, prices in Hebei's Tangshan, Qian'an, and Qianxi regions increased by 5-10 yuan/mt, while prices in west Liaoning's Chaoyang, Beipiao, and Jianping regions rose by 5-10 yuan/mt. Prices in east China increased by 20-30 yuan/mt.

Tangshan RegionIron ore concentrate prices remained relatively stable, with the delivery-to-factory price of Fe66% iron ore concentrates (dry basis, tax-included) at 960-970 yuan/mt. The local iron ore market has not fully resumed operations, and iron ore resources remain tight. Steel mills' overall purchase willingness was weak, with most opting to observe the market before restocking, leading to a relatively quiet market.

West Liaoning RegionThe price of Fe66% iron ore concentrates (wet basis, tax-excluded) was 700-710 yuan/mt. Currently, demand in the west Liaoning domestic ore market is weak, and traders' inquiries and offers are mostly tentative. Additionally, beneficiation plants resumed production at a slow pace after the holiday and were not in a hurry to quote or sell, keeping market prices stable compared to pre-holiday levels. Overall, supply remains tight, providing some support for local iron ore concentrate prices.

East China RegionMines and beneficiation plants gradually resumed normal production, but some remained shut down due to the holiday, keeping overall resources tight. On the demand side, steel mills showed some restocking demand, which may drive transactions of local iron ore concentrates.

Considering both domestic and imported ore prices, imported ore prices rose significantly this week, narrowing the price spread between domestic and imported ore. The price spread may widen again next week.

Outlook for Next Week

For imported ore:Recently, frequent cyclones in the Southern Hemisphere have affected shipments from Australian ports, and global iron ore shipments are expected to decrease again. Meanwhile, a new cold wave in China may reduce port unloading efficiency, making it difficult for port arrivals to increase significantly. On the demand side, the pace of steel mills resuming production is slowing, and pig iron production is expected to decline slightly next week, with iron ore demand remaining stable with a weak trend. Overall, the supply-demand imbalance in the industry chain is not prominent, and with the enhanced policy expectations from the Two Sessions, iron ore prices are expected to hover at highs next week.

For domestic ore:Overall, due to the impact of the Chinese New Year holiday, domestic iron ore concentrate resources remain tight in the short term, providing some support for domestic ore prices. On the demand side, steel mills are expected to restock after the holiday, which may drive market transactions. Coupled with the recent upward trend in iron ore futures, domestic iron ore concentrate prices are expected to have some room for further increases next week.

Click to View the SMM Metal Industry Chain Database