》View SMM Aluminum Product Prices, Data, and Market Analysis

》Subscribe to Access Historical SMM Metal Spot Prices

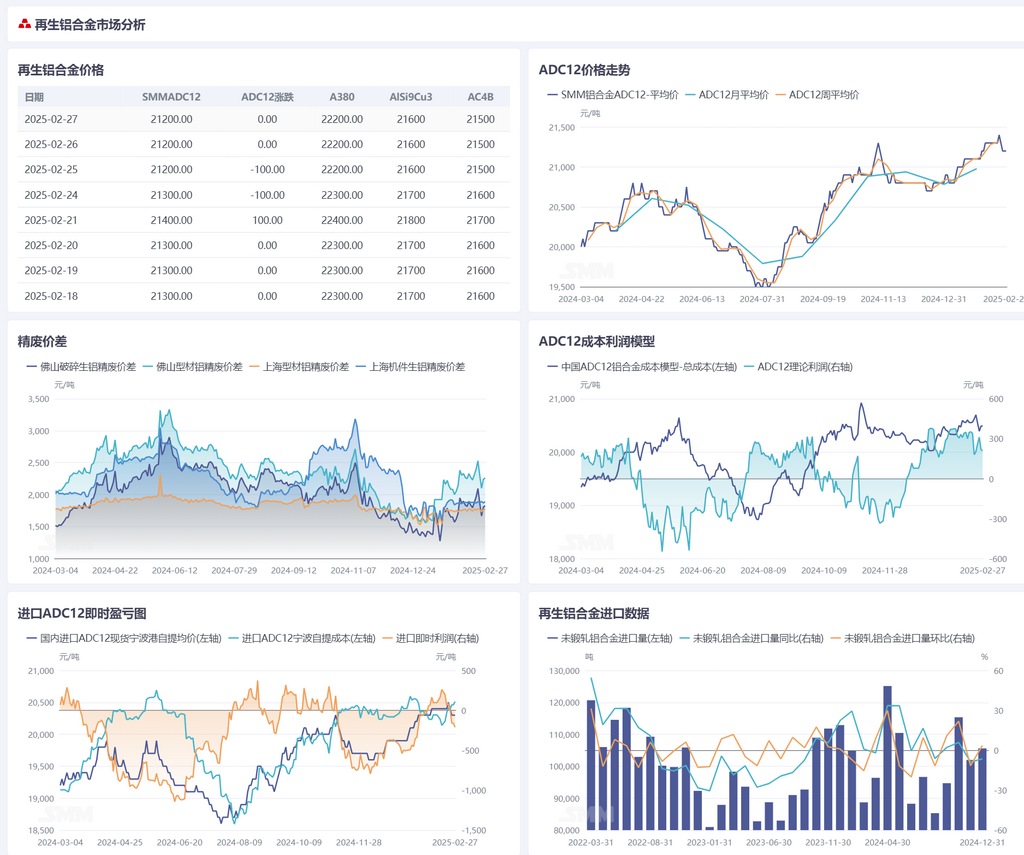

Secondary Aluminum Raw Materials:

This week, downstream purchasing gradually resumed. However, constrained by high prices and the lack of significant improvement in downstream demand, the market maintained purchasing as needed. During the period, aluminum scrap prices fluctuated in line with aluminum prices. Considering the moderate downstream purchasing willingness, aluminum scrap price fluctuations were limited. Mid-week, as the price center of primary aluminum adjusted downward, the price difference between primary metal and scrap fluctuated rangebound. In terms of aluminum scrap supply, post-holiday resumption of production and new orders received by aluminum processing enterprises led to a steady recovery in new scrap supply. Regarding overseas aluminum scrap supply, due to the impact of the price spread between domestic and overseas markets, significant improvement was limited. SMM will continue to monitor changes in import policies for aluminum scrap. As of this Thursday, SMM A00 spot price was reported at 20,550 yuan/mt, down 50 yuan/mt WoW. Shanghai aluminum tense scrap price was 18,662 yuan/mt, down 163 yuan/mt WoW. The price difference between A00 aluminum and Shanghai aluminum tense scrap expanded by 23 yuan/mt WoW to 1,888 yuan/mt. The price difference between A00 aluminum and Foshan aluminum extrusion scrap narrowed by 1,400 yuan/mt WoW to 2,258 yuan/mt. In the short term, the domestic aluminum scrap market supply and demand are both in a recovery phase. Recently, primary aluminum prices have fluctuated significantly, with aluminum scrap prices adjusting accordingly. Considering the upcoming "Golden March and Silver April," downstream demand may improve, and aluminum scrap prices are expected to fluctuate at highs.

Secondary Aluminum Alloy:

This week, domestic ADC12 secondary aluminum alloy prices showed a trend of initial decline followed by stabilization, with a cumulative decrease of 200 yuan/mt during the week to the range of 21,200 yuan/mt. On the cost side, although aluminum scrap prices slightly declined due to primary aluminum price fluctuations, the tight supply pattern supported bottom resilience. Meanwhile, above-standard #553 silicon prices continued to drop by 100 yuan/mt to 10,650 yuan/mt, further alleviating alloy cost pressure. On the demand side, the resumption pace of downstream die-casting enterprises fell short of expectations, and orders in sectors such as automotive recovered slowly. Downstream purchasing was mainly for restocking as needed, and overall market transactions remained weak. The lack of growth drivers on the demand side, coupled with intensified aluminum price fluctuations, heightened downstream sentiment of wait-and-see, significantly reducing the momentum for price increases during the week. On the supply side, post-holiday operating rates of secondary aluminum enterprises have gradually returned to normal levels, with a noticeable increase in market supply. However, insufficient follow-up of downstream orders led to continued accumulation of social and production site inventory. In terms of imports, overseas ADC12 prices rose to $2,480-2,500/mt. Due to the decline in domestic prices, the immediate profit and loss of ADC12 imports turned into a slight loss, closing the import window. While this eased external supply pressure, the domestic supply surplus pattern remained unchanged, limiting the room for price rebound. Overall, the ADC12 market is expected to continue fluctuating rangebound after March. Although the traditional consumption peak season is approaching, caution is needed as ADC12 prices may face further short-term downward pressure if end-use consumption recovery falls short of expectations. However, with cost support, the downside is expected to be limited.