[SMM Analysis]Market Rumors Disrupt, Ningbo HRC Demand Falls Short of Expectations

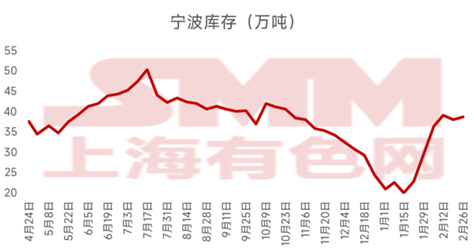

According to the SMM survey, this week, SMM's large-scale inventory of Ningbo HRC stood at 388,300 mt (as of February 26), up 7,400 mt WoW.

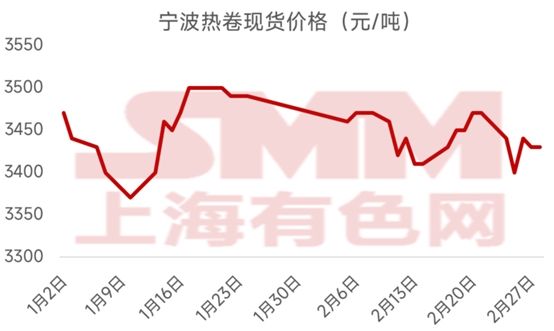

This week, HRC futures prices first declined and then rebounded. As of the afternoon close on February 28, the most-traded HRC 2505 contract settled at 3,425 yuan/mt. This week, the market was significantly affected by rumors of anti-dumping measures, crude steel output control, and macroeconomic meetings, leading to notable fluctuations in the futures market. Ultimately, spot prices in most major cities fell by 20-60 yuan/mt WoW. Market trading sentiment varied with futures market movements. On Friday, trading in east and south China was moderate, while it was average in north China.

According to the SMM survey, in Ningbo's spot trading market this week, transaction prices of mainstream HRC resources fluctuated rangebound. As of the afternoon of February 28, late-session spot prices were quoted at 3,430-3,440 yuan/mt, down from last Friday's 3,470 yuan/mt by 30-40 yuan/mt. This week, the spot market saw moderate trading activity, with better performance mid-week but a pullback in the latter half, as market sentiment cooled and downstream buyers mostly adopted a wait-and-see approach. Ningbo's HRC inventory increased this week, with spot market demand falling short of expectations. Some traders reported that the rapid rise in futures prices failed to drive significant spot transactions. As of mid-week (February 26), inventory rose by 7,400 mt WoW. With macroeconomic meetings approaching, market speculation may continue to drive a rebound in futures prices. Demand release is expected to remain moderate next week, and Ningbo's inventory may decline again.

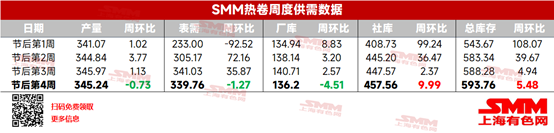

This week, SMM's weekly balance data showed that HRC production slightly decreased due to equipment maintenance, such as rolling mills, at some steel mills in north China. In terms of market trends, futures prices first declined and then rebounded this week. Earlier, the anti-dumping measures significantly suppressed futures prices, dampening market purchasing enthusiasm and accelerating inventory buildup. Except for slight inventory declines in central and northeast China, inventories in east, south, and north China all increased. Currently, the total national HRC inventory stands at 4.0925 million mt, up 49,100 mt WoW, an increase of 1.21% WoW but a decrease of 8.21% YoY. Looking ahead, some steel mills are showing increased willingness to conduct additional maintenance, which may further ease supply pressure. Meanwhile, with the Two Sessions approaching and the fading impact of anti-dumping sentiment, suppressed end-use demand is expected to gradually recover. Therefore, national inventory is expected to start declining next week.