This week, a turning point in total construction steel inventory was observed, with both rebar and wire rod inventories shifting from an increasing to a decreasing trend. Rebar total inventory declined 0.45% WoW, while wire rod total inventory dropped 0.59% WoW. On the supply side, due to a major conference, some regions received short-term environmental protection-driven production restrictions, leading to temporary shutdowns of blast furnaces and a slight decrease in pig iron production. This period saw three additional electric furnace plants resuming operations, with the operating rate of electric furnaces rising 3.08% WoW. Currently, all EAF steel mills, except for those under long-term or short-term shutdown, have resumed production. On the demand side, downstream demand has gradually recovered, with projects in south China progressing faster than in the north, resulting in a moderate increase in market demand. This week, total construction steel inventory shifted from an increasing to a decreasing trend.

This week, the total rebar inventory stood at 8.0352 million mt, down 36,200 mt WoW, a decline of 0.45% (previous: +1.76%), and 4.3499 million mt YoY, a 35.12% decline (previous: -34.42%).

Table 1: Overview of Rebar Inventory Conditions

Data Source: SMM

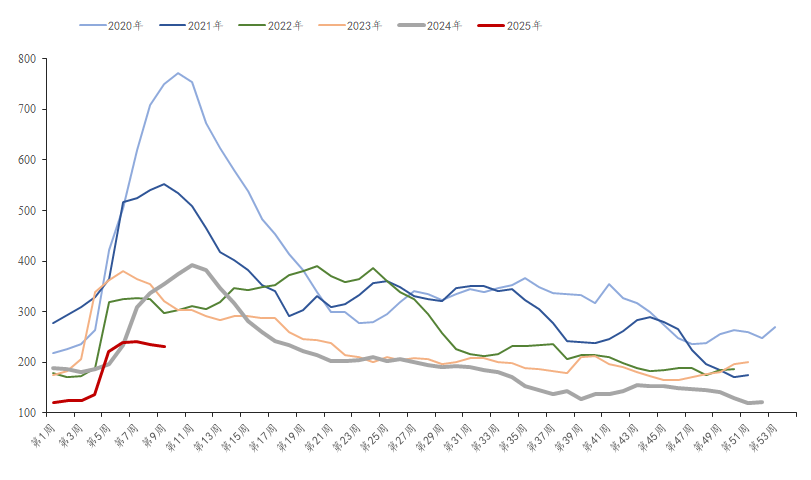

This week, in-plant rebar inventory was 2.3083 million mt, a decrease of 52,200 mt WoW, a 2.21% decline (previous: -2.23%), and 1.6163 million mt YoY, a 41.18% decline (previous: -36.99%). With the gradual resumption of downstream activities, end-use demand is steadily being released, and direct shipments from steel mills are increasing, leading to a shift from an increasing to a decreasing trend in in-plant inventory.

Chart-1: Trend of Rebar In-Plant Inventory 2020-2025

Data Source: SMM

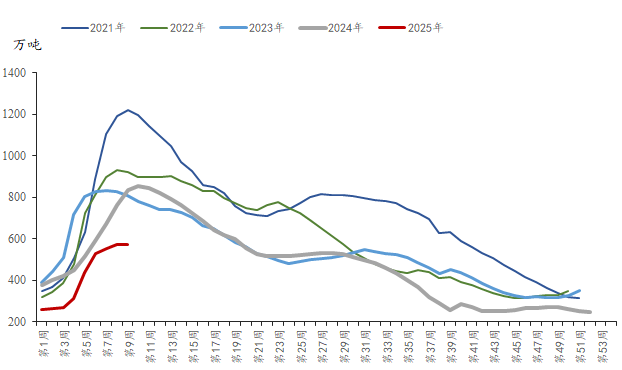

This week, social rebar inventory was 5.7269 million mt, up 16,000 mt WoW, a 0.28% increase (previous: +3.51%), and down 2.7336 million mt YoY, a 32.31% decline (previous: -33.3%). As downstream terminals gradually resume operations, the market's intention to purchase low-priced resources is moderate. Although social inventory still increased this week, the growth rate has significantly narrowed.

Chart-2: Trend of Rebar Social Inventory 2021-2025

Data Source: SMM

Overall, downstream demand has gradually recovered, with projects in south China progressing faster than in the north. Total construction steel inventory has shifted from an increasing to a decreasing trend, and fundamental imbalances are not yet prominent. As the weather warms, downstream construction progress will accelerate, and it is expected that total construction steel inventory will continue to decline. Subsequently, close attention should be paid to any changes in macro policies after the major conference and the sustainability of downstream demand.