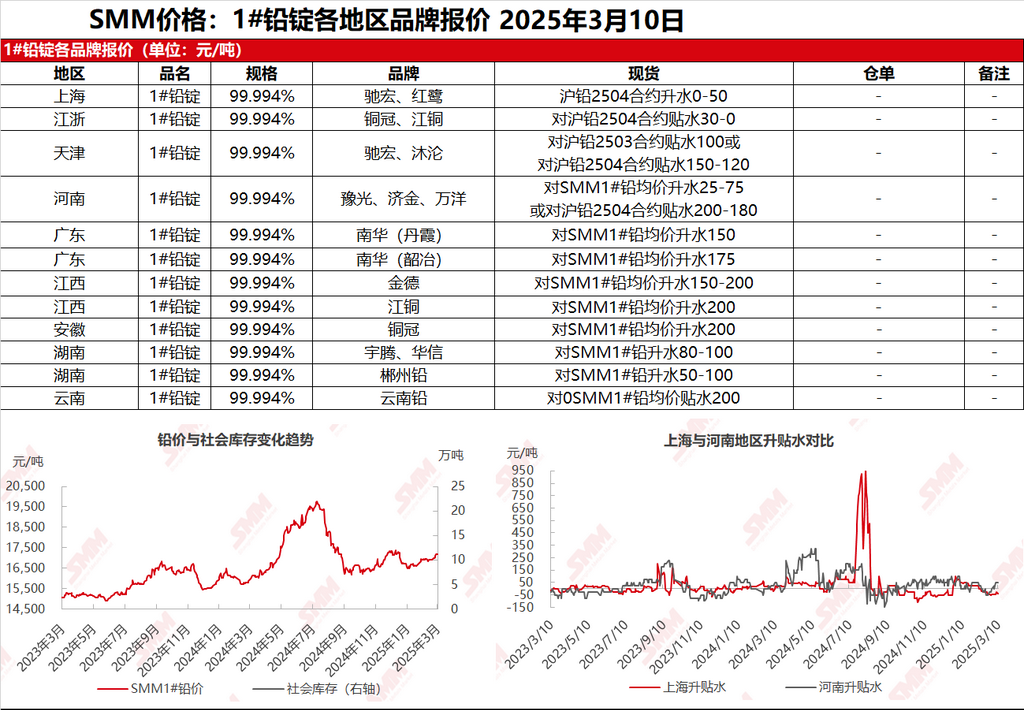

SMM, March 10: In the Shanghai market, Chihong lead was quoted at 17,480-17,520 yuan/mt, with a premium of 0-50 yuan/mt against the SHFE lead 2504 contract. Honglu lead was quoted at 17,430-17,470 yuan/mt, on par with the SHFE lead 2504 contract. In Jiangsu and Zhejiang regions, Tongguan and JCC lead were quoted at 17,400-17,470 yuan/mt, with a discount of 30-0 yuan/mt against the SHFE lead 2504 contract. SHFE lead fluctuated upward, and suppliers adjusted their quotes according to market trends. Some suppliers awaited delivery, keeping their quotes relatively firm. Meanwhile, cargoes self-picked up from production sites were limited, and the northern market was still under smog-related production and traffic restrictions. Suppliers' premiums rose slightly WoW (against the SMM 1# lead average price). Additionally, secondary lead smelters stood firm on quotes, with secondary refined lead ex-factory at a discount of 75-0 yuan/mt against the SMM 1# lead average price, and a few even at a premium of 50-75 yuan/mt. Downstream enterprises mainly purchased through long-term contracts, while spot orders were limited to just-in-time procurement.

Other markets: Today, the SMM 1# lead price fell by 25 yuan/mt compared to the previous trading day. In Henan, smelters quoted a premium of 50-100 yuan/mt against the SMM 1# lead average price or a discount of 160-180 yuan/mt against the SHFE lead 2504 contract ex-factory. In Hunan, branded lead smelters quoted a premium of 50-100 yuan/mt against the SMM 1# lead average price, with just-in-time procurement transactions. In Yunnan, the discount against the SMM 1# lead average price remained at 200 yuan/mt. Lead prices weakened slightly, smelters raised premiums, and downstream buyers made limited just-in-time procurements while maintaining a wait-and-see approach. Market transactions were relatively sluggish.