1. According to the SMM survey, coke profit this week was 1.3 yuan/mt, with most coke enterprises operating near the break-even point.

From a pricing perspective, the eleventh round of coke price cuts occurred this week, negatively impacting coke profit margins. From a cost perspective, coal mines maintained normal production recently, with coking coal supply remaining high. Additionally, due to the decline in coke prices, some coal types saw early price reductions, which helped restore coke enterprises' profitability, preventing most from incurring losses.

Next week, some market participants still hold bearish expectations for coke prices. However, coking coal prices may experience supplementary declines, reducing coking costs and offsetting the impact of falling coke prices. Most coke enterprises are expected to continue hovering near the break-even point.

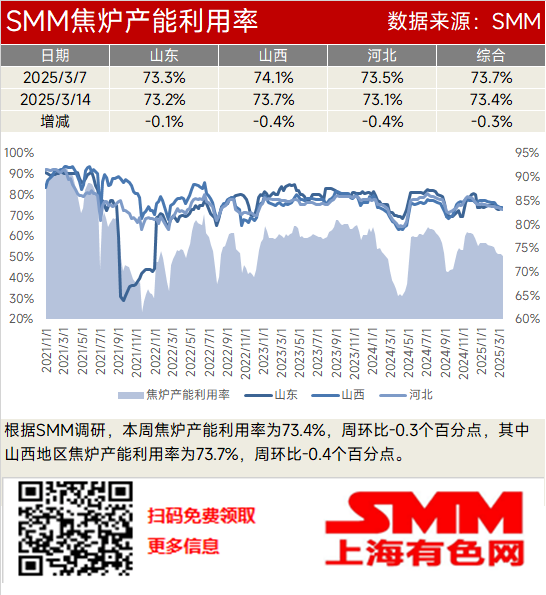

2. According to the SMM survey, the coke oven capacity utilisation rate this week was 73.4%, down 0.3 percentage points WoW. In Shanxi, the coke oven capacity utilisation rate was 73.7%, down 0.4 percentage points WoW.

From a profitability perspective, most coke enterprises were at the break-even point or slightly in deficit, with minimal impact on production. From an inventory perspective, shipment pressure on coke enterprises eased, and overall coke inventory continued to decline, reducing the negative impact on production enthusiasm.

Subsequently, most coke enterprises may face losses, but within a tolerable range, with only a small number reducing production. Coke supply is expected to decrease slightly. Meanwhile, the gradual recovery of the end-use market has increased demand for steel, driving up pig iron production at steel mills and daily coke consumption. Some steel mills have started purchasing. In summary, while the fundamentals of the coke market have improved, they remain relatively loose. Additionally, high coke inventories at coke enterprises continue to suppress production enthusiasm. The coke oven capacity utilisation rate at coke enterprises is expected to decline slightly next week.

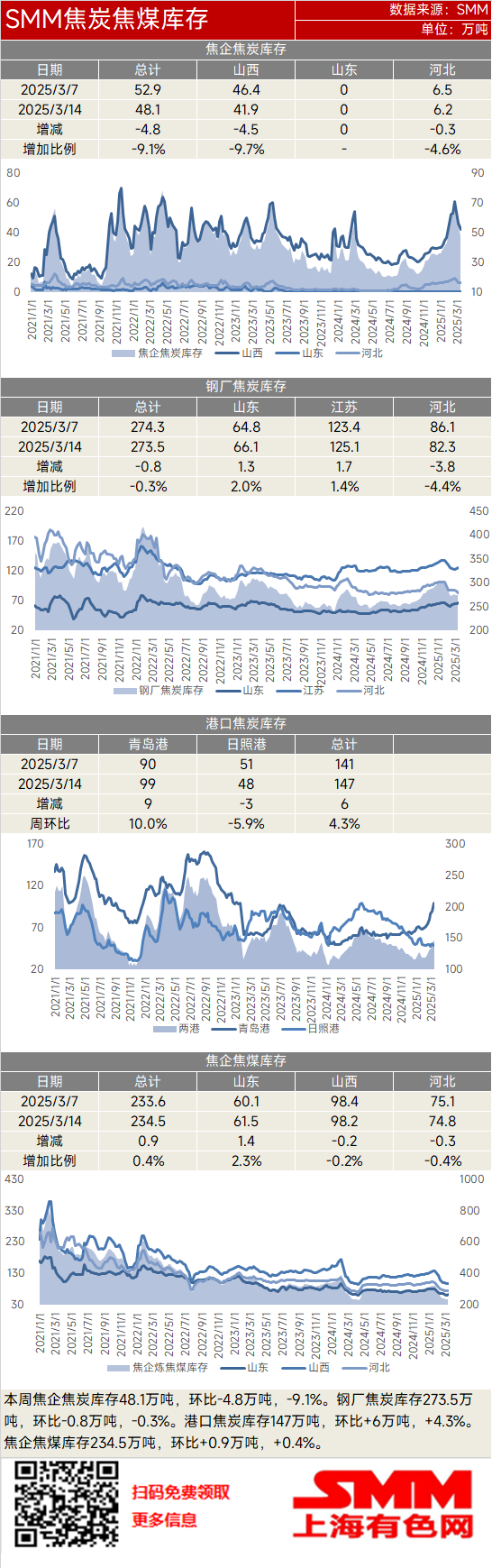

3. This week, coke inventory at coke enterprises was 481,000 mt, down 48,000 mt (-9.1%) WoW. Coke inventory at steel mills was 2.735 million mt, down 8,000 mt (-0.3%) WoW. Coke inventory at ports was 1.47 million mt, up 60,000 mt (+4.3%) WoW. Coking coal inventory at coke enterprises was 2.345 million mt, up 9,000 mt (+0.4%) WoW.

This week, coke enterprises continued destocking coke inventory, while coke inventory at steel mills fluctuated rangebound. Some coke enterprises incurred losses, reducing production enthusiasm and tightening coke supply. Meanwhile, improved sales of finished steel at steel mills boosted production enthusiasm, prompting some mills with low coke inventories to restock slightly, thereby reducing inventory pressure on coke enterprises. The steel market performed moderately this week, with increased purchasing enthusiasm among some low-inventory steel mills. However, rumors of detailed rules for crude steel production cuts being issued on March 15 led most steel mills to adopt a wait-and-see sentiment, primarily purchasing coke as needed.

Subsequently, some coke enterprises may continue to reduce production, tightening coke supply. However, if detailed rules for crude steel production cuts are issued on March 15, pig iron production at steel mills may decline, reducing daily coke consumption. Additionally, with steel mills' coke inventories remaining moderate, they are expected to continue purchasing coke as needed. Next week, coke enterprises are expected to continue destocking, while coke inventory at steel mills is likely to fluctuate rangebound.

This week, coke supply began to tighten, with limited room for further cost reductions. Combined with coke enterprises transferring coke inventory to ports, coke inventory at ports is expected to increase next week.

This week, coking coal inventory at coke enterprises fluctuated rangebound. The primary reason is that after a prolonged period of continuous price declines, coking coal prices have limited room for further decreases and are falling at a slower pace. Even though downstream acceptance of current coking coal prices remains low, significant further price drops are unlikely. Some coke enterprises with low coking coal inventories have started purchasing. Subsequently, with limited room for further price declines and some coke enterprises having restocking needs, purchasing enthusiasm is expected to increase. Coking coal inventory at coke enterprises is expected to stop declining and increase slightly next week.