SMM March 19 News:

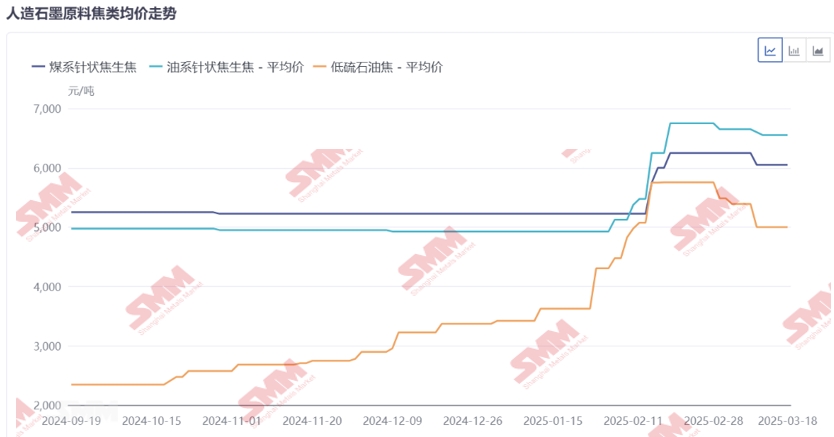

Cost side, anode raw materials include petroleum coke and needle coke. Petroleum coke prices surged sharply after the Chinese New Year holiday, primarily due to tight petroleum coke supply and active restocking by downstream enterprises after the holiday. Needle coke prices increased mainly driven by high costs and restricted import volumes.

From the cost side of anode raw material coke, regarding tariffs, starting from January 2025, the import tariff on fuel oil will be adjusted from 1% to 3%. Regarding consumption tax, the deductible proportion of fuel oil consumption tax will be reduced from 100% to 50%-60%. According to SMM market surveys, this series of tax policy adjustments will lead to an increase in costs for petroleum coke and needle coke producers by 600-700 yuan/mt.

From the supply side of anode raw material coke, in terms of imports, restrictions on docking and unloading of import vessels at some ports in Shandong have directly hindered petroleum coke and needle coke producers in obtaining raw materials, leading to an increase in import costs. Regarding production, many petroleum coke refineries are currently undergoing maintenance cycles after the year-end. According to SMM, this maintenance is a major overhaul conducted every five years, with the longest maintenance period lasting six months. Among the enterprises undergoing maintenance, 41% are low- and mid-sulphur petroleum coke producers. Regarding new capacity expansion, SMM reports that low- and mid-sulphur petroleum coke producers currently have limited expansion plans, and petroleum coke supply is expected to remain tight in the short term.

From the demand side of anode raw material coke, it can be analyzed from the perspectives of downstream anode demand and traditional industry demand. Anode enterprises, having undergone significant destocking in Q4, are currently at low inventory levels. Coupled with the rapid growth in the end-use market after the new year, anode enterprises have shown strong restocking intentions as the market gradually recovers post-holiday. In traditional industries, due to environmental protection policies, the demand for petroleum coke in anodes is gradually shifting from high-sulphur to low-sulphur grades, leading to an increase in purchases of low-sulphur petroleum coke. Additionally, the demand for pre-baked anodes and anodes in 2025 is expected to increase, further boosting petroleum coke sales.

In summary, for petroleum coke, under the backdrop of high costs, tight supply, and rising demand, petroleum coke prices have seen a significant surge. However, due to the high volatility of petroleum coke prices recently, downstream purchasing enthusiasm has weakened, leading to a certain degree of pullback in petroleum coke prices. Nevertheless, the pullback is not as significant as the previous surge, and overall, petroleum coke prices in Q1 still show an upward trend. For needle coke, as prices were previously in a low range, they have risen to a certain extent driven by high costs, and needle coke producers currently exhibit a strong sentiment to stand firm on quotes.

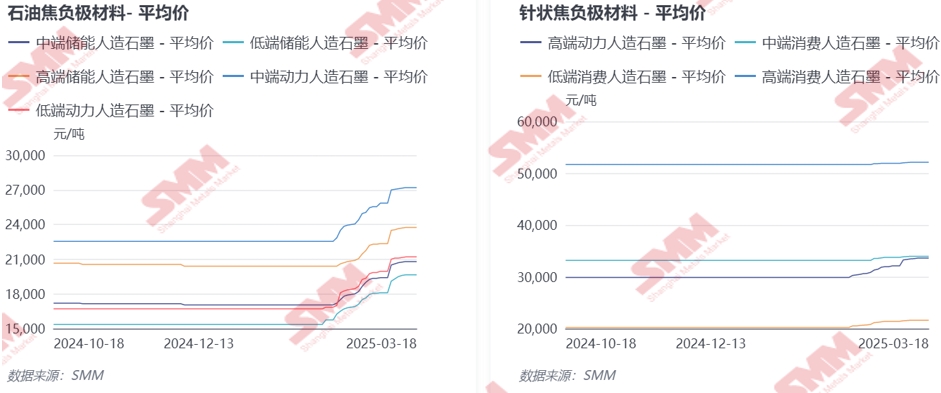

Artificial graphite prices showed a clear upward trend in February and early March. Cost side, in addition to the impact of the aforementioned raw material coke price increases, graphitisation outsourcing enterprises have seen profits fall below cost lines. Therefore, under the backdrop of demand recovery after the Chinese New Year, these enterprises have shown a growing sentiment to stand firm on quotes, with Acheson furnace prices showing a slight upward trend in March. Supply side, under the pressure of high costs and the situation where profits for some graphite materials have fallen below cost lines, the production enthusiasm of anode enterprises has declined. Additionally, due to the impact of the holiday, imports of anode materials have been somewhat reduced due to logistical disruptions, leading to a certain degree of decline in the overall supply of anode materials. Demand side, the operating rate of downstream battery cell enterprises has increased after the Chinese New Year, driving up demand for key anode materials. In summary, the theoretical costs of anode materials have risen significantly, threatening the survival space of anode material enterprises. Production enthusiasm among these enterprises remains low, but due to the ongoing restocking demand from battery cells, anode material prices have recently shown a certain degree of increase. Specifically, low-end artificial graphite for ESS prices rose by 28%, mid-end artificial graphite for ESS by 22%, high-end artificial graphite for ESS by 16%, low-end artificial graphite for NEV by 27%, mid-end artificial graphite for NEV by 21%, high-end artificial graphite for NEV by 13%, low-end artificial graphite for consumer electronics by 7%, mid-end artificial graphite for consumer electronics by 2%, and high-end artificial graphite for consumer electronics by 1%.

Looking ahead, for petroleum coke, as of March 19, low-sulphur petroleum coke prices have pulled back by approximately 22% after a new round of price reductions. Many petroleum coke producers have adopted price protection sales strategies, and prices may continue to decline further. However, due to the ongoing impact of tax policies, the extent of future price reductions may be very limited, making it difficult to return to the pre-increase price range. For needle coke, in the absence of significant changes in the supply-demand relationship, prices are expected to remain firm due to their previous low range. For graphitisation, as market recovery drives demand growth, the tight oversupply situation may ease but is unlikely to reverse. Therefore, under the backdrop of profits falling below cost lines, graphitisation prices are expected to remain relatively stagnant. For anode materials, although prices have recently shown some pullback, anode material production still relies on high-cost raw material coke due to production lag. With limited room for cost reductions, anode materials are expected to be sold at stable prices in the short term.

SMM New Energy Research Team

Cong Wang 021-51666838

Xiaodan Yu 021-20707870

Rui Ma 021-51595780

Disheng Feng 021-51666714

Yujun Liu 021-20707895

Yanlin Lü 021-20707875

Zhicheng Zhou 021-51666711

Haohan Zhang 021-51666752

Zihan Wang 021-51666914

Xiaoxuan Ren 021-20707866

Jie Wang 021-51595902

Yang Xu 021-51666760

Mengqi Xu 021-20707868