Check SMM Aluminum Product Prices, Data, and Market Analysis

Order to View SMM Metal Spot Historical Prices

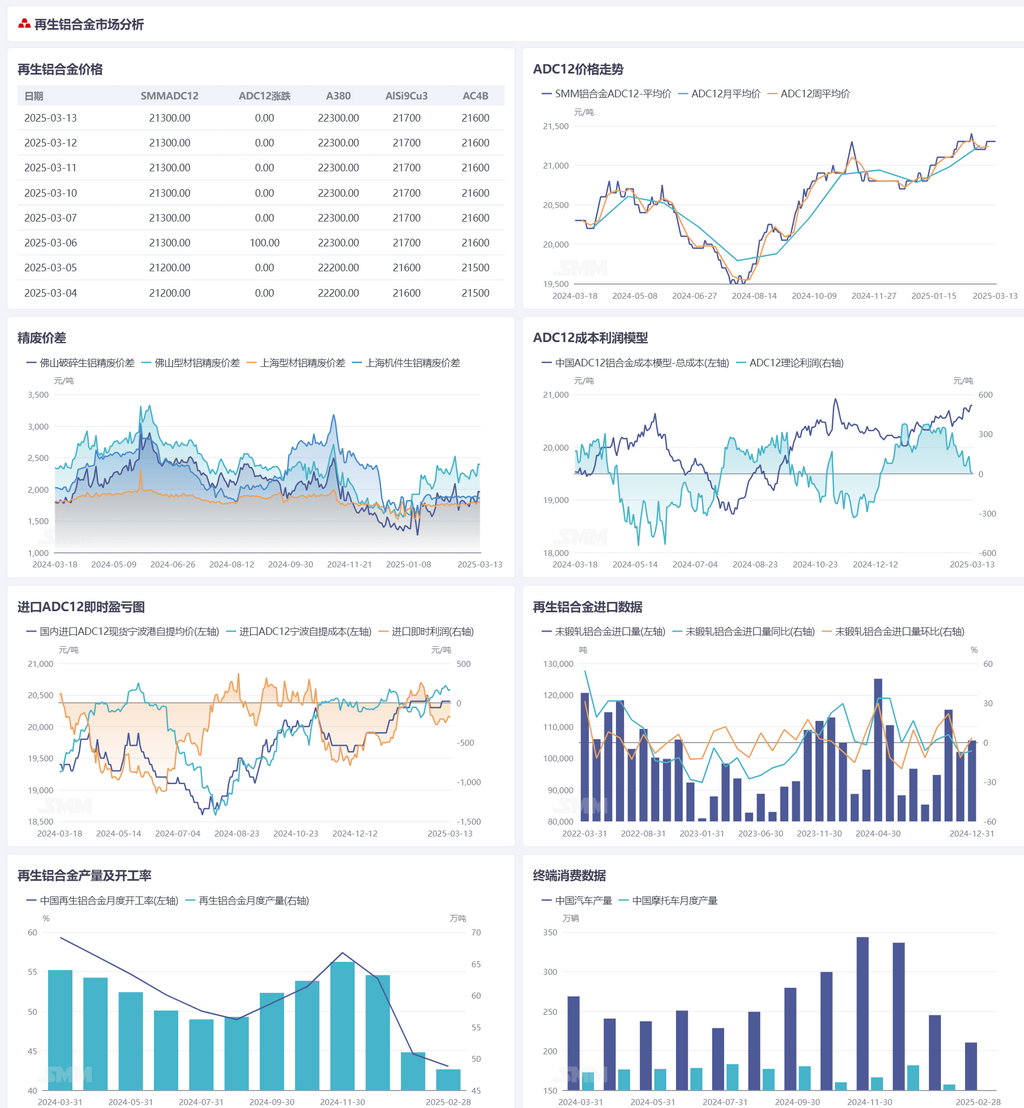

Secondary Aluminum Raw Material:

This week, aluminum scrap prices followed the volatility of primary aluminum, with a somewhat muted market response. This was mainly due to the lack of significant improvement in downstream alloy ingot demand, with the market purchasing as needed, and the price difference between primary metal and scrap fluctuating. In terms of aluminum scrap supply, with the arrival of the peak consumption season in March and April, the operating rate of the aluminum processing industry is generally in a recovery phase, and new scrap supply has shown some improvement. Regarding overseas aluminum scrap supply, the price spread between domestic and overseas markets still exists, and recent tightening of export policies for scrap aluminum in Southeast Asia may cause disruptions in imported scrap aluminum supply. SMM will continue to monitor changes in the industry. As of Thursday this week, SMM A00 spot prices were at 20,810 yuan/mt, down 100 yuan/mt WoW; Shanghai machine parts aluminum tense scrap prices were at 18,933 yuan/mt, down 109 yuan/mt WoW, and the price difference between A00 aluminum and Shanghai machine parts aluminum tense scrap rose by 9 yuan/mt WoW to 1,877 yuan/mt; the price difference between A00 aluminum and Foshan aluminum extrusion scrap fell by 90 yuan/mt WoW to 2,301 yuan/mt. In the short term, domestic aluminum scrap market prices are expected to follow the volatility of primary aluminum, with no significant improvement in downstream demand, and the market will maintain purchasing as needed. The price difference between primary metal and scrap is expected to fluctuate next week.

Secondary Aluminum Alloy:

This week, aluminum prices first declined then rebounded, while secondary aluminum alloy prices remained more likely to fall than rise. As of March 20, SMM ADC12 prices decreased by 100 yuan/mt WoW to 21,200 yuan/mt. On the demand side, halfway through March, end-use consumption in the secondary aluminum market remains sluggish. Many die-casting companies reported a significant YoY decline in orders in March, leading to a reduction in orders for secondary aluminum plants. Additionally, with volatile aluminum prices, downstream buyers maintained a just-in-time procurement strategy, refraining from stockpiling. Under the pressure of weak demand and increasingly fierce market competition, the market struggled to catch up on price increases but quickly followed declines. In terms of supply, the "Golden March" peak season expectations have not materialized, and the operating levels of secondary aluminum plants have fallen short of expectations, making it difficult to meet the production targets set at the beginning of the month. Slow sales have led to a continuous accumulation of finished product inventories. Although the theoretical profit margin for the ADC12 industry is still positive, if the market continues to be depressed, the industry could fall into losses, and production cuts would become inevitable, potentially alleviating some of the supply-side pressure. In terms of imports, overseas ADC12 prices remain strong, currently at $2,500-2,540/mt, while domestic prices are under downward pressure, causing the immediate import loss to widen to 300-500 yuan/mt, keeping the import window closed. In summary, the current secondary aluminum alloy market faces a prominent supply-demand imbalance, and in the short term, ADC12 prices are likely to continue to be more likely to fall than rise.