Futures Market: LME copper was closed overnight. The most-traded SHFE copper 2502 contract opened at 74,580 yuan/mt, initially hitting a high of 74,690 yuan/mt before fluctuating downward to an intraday low of 74,380 yuan/mt. It then fluctuated rangebound and consolidated at the end of the session, finally closing at 74,430 yuan/mt, up 0.36%. Trading volume reached 19,000 lots, and open interest stood at 143,000 lots.

【SMM Copper Morning Brief】News: (1) According to the national economic accounting system and international practices, the National Bureau of Statistics (NBS) revised the GDP for the census year (2023) using data from the Fifth National Economic Census and relevant departmental information, while simultaneously implementing a reform in the accounting method for urban residents' self-owned housing services. The revised GDP for 2023 is 129,427.2 billion yuan, an increase of 3,369 billion yuan from the preliminary estimate, representing a growth rate of 2.7%. (2) Local governments have intensified efforts to promote a new round of trade-in policies for consumer goods and large-scale equipment upgrades, aiming to expand and enhance consumption. Data shows that since the beginning of this year, trade-in policies for consumer goods have driven related product sales exceeding 1 trillion yuan. Production of NEVs, household freezers, and other products related to trade-in policies has maintained rapid growth.

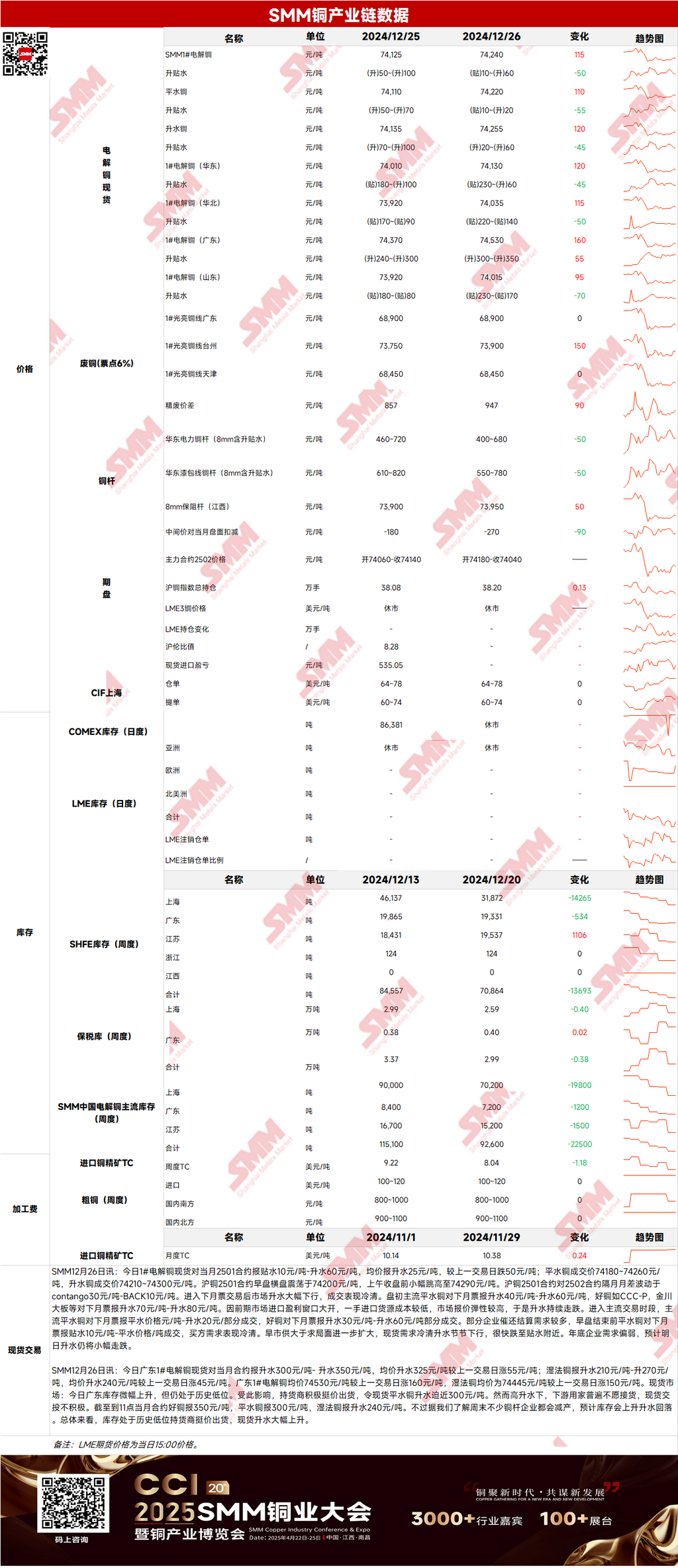

Spot Market: (1) Shanghai: On December 26, #1 copper cathode spot prices against the front-month 2501 contract were quoted at a discount of 10 yuan/mt to a premium of 60 yuan/mt, with an average premium of 25 yuan/mt, down 50 yuan/mt WoW. As trading shifted to cargoes with invoices dated next month, spot premiums fell sharply, and transactions were sluggish. The oversupply situation further intensified, with weak spot demand causing premiums to decline rapidly, approaching discounts. Year-end demand from enterprises remained weak, and spot premiums are expected to decline slightly today. (2) Guangdong: On December 26, #1 copper cathode spot prices against the front-month contract were quoted at premiums of 300-350 yuan/mt, with an average premium of 325 yuan/mt, up 55 yuan/mt WoW. Overall, inventory remained at historically low levels, and suppliers stood firm on quotes, leading to a significant increase in spot premiums. (3) Imported Copper: On December 26, warehouse warrant prices were $64-78/mt, QP January, with the average price flat WoW; B/L prices were $60-74/mt, QP January, with the average price flat WoW; EQ copper (CIF B/L) was quoted at $14-28/mt, QP January, with the average price flat WoW. Quotes referenced cargoes arriving in late December and early January. LME copper remained closed yesterday, leaving no overseas market reference. The US dollar-denominated copper market was quiet, with few offers seen. (4) Secondary Copper: On December 26, secondary copper raw material prices remained unchanged MoM. Guangdong bare bright copper prices were 68,800-69,000 yuan/mt, unchanged MoM. The price difference between primary metal and scrap was 947 yuan/mt, up 90 yuan/mt MoM. The price spread between primary and secondary copper rods was 810 yuan/mt. According to the SMM survey, with the new policy implementation approaching, some secondary copper raw material suppliers were concerned about price suppression by secondary copper rod plants after the New Year holiday. As a result, they actively sold off inventory, delivering secondary copper raw materials to reputable factories. Some factories reported purchasing nearly 60 truckloads of secondary copper raw materials today and issued stop-purchase notices due to concerns over excessive inventory. (5) Inventory: On December 26, LME copper cathode inventory remained unchanged at 272,725 mt. SHFE warehouse warrant inventory decreased by 1,598 mt to 13,061 mt.

Prices: Macro side, Thursday's data showed that the number of Americans filing new claims for unemployment benefits last week fell to the lowest level in a month, consistent with a cooling but still healthy US labour market. Additionally, post-Christmas holiday trading was sluggish, and the US dollar index edged down but remained at high levels, mainly due to market expectations that the US dollar will be supported by Trump administration policies next year, limiting copper price gains. Fundamentals side, the earlier opening of the import arbitrage window led to low-cost imported cargoes, resulting in ample copper cathode spot supply. However, year-end downstream demand remained weak, and overall transactions were sluggish. As of Thursday, December 26, SMM copper inventories in major regions nationwide increased by 6,000 mt from Monday to 105,400 mt, up 6,700 mt WoW, ending nine consecutive weeks of decline with a slight rebound. Compared to Monday's inventory changes, most regions nationwide saw increases, with only Guangdong and Jiangsu experiencing slight declines. Total inventory was 39,000 mt higher than the 66,400 mt YoY. In terms of prices, the macro outlook remains bearish, and fundamentals lack support, suggesting copper prices are expected to lack upward momentum today.

》Click to View the SMM Metal Database

【The above information is based on market data and comprehensive assessments by the SMM research team. The information provided is for reference only and does not constitute direct investment research advice. Clients should make cautious decisions and not substitute this for independent judgment. Any decisions made by clients are unrelated to SMM.】