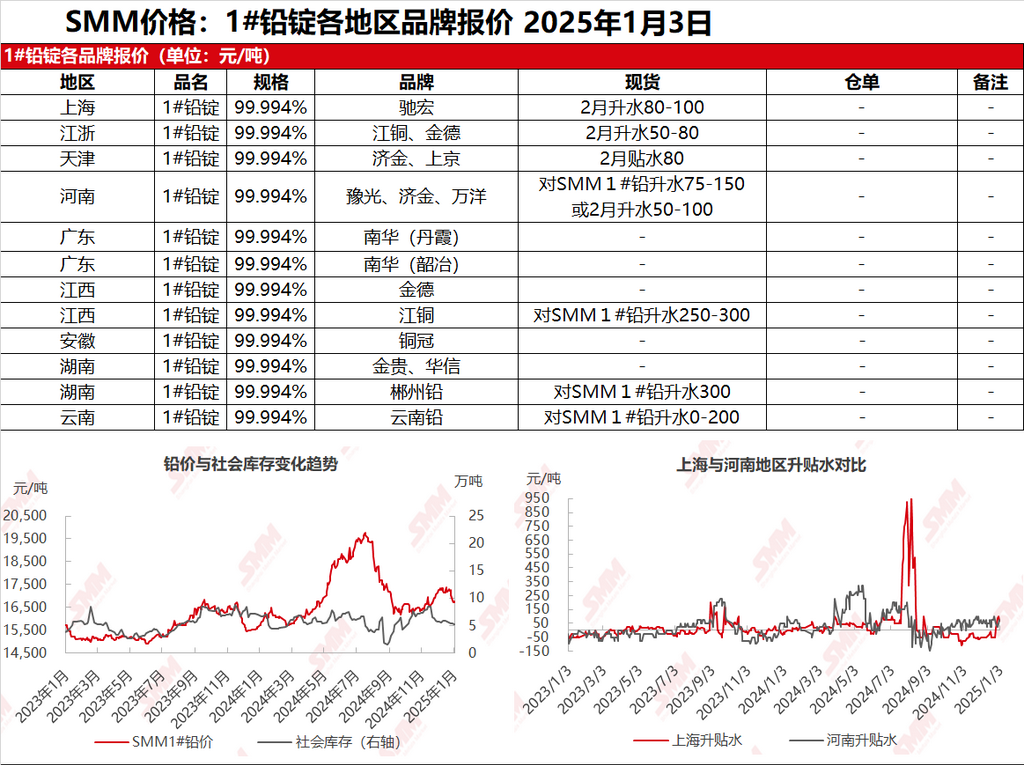

SMM reported on January 3: In the Shanghai market, Chihong lead was quoted at 16,770-16,815 yuan/mt, with spot premiums of 80-100 yuan/mt against the SHFE lead 2502 contract. In Jiangsu and Zhejiang regions, JCC and Jinde lead were quoted at 16,740-16,800 yuan/mt, with spot premiums of 50-80 yuan/mt against the SHFE lead 2502 contract. The center of SHFE lead prices shifted downward, and suppliers showed moderate enthusiasm for shipments. During this period, smog warnings were reissued in Henan and Anhui regions, restricting some primary and secondary lead smelting production and lead ingot transportation. Quotations from primary lead smelters decreased, while premiums (against the SMM 1# lead average price) were raised. Meanwhile, secondary lead quotations significantly declined, and downstream enterprises exhibited strong wait-and-see sentiment, with some making just-in-time procurement.

Other markets: Today, the SMM 1# lead price dropped by 75 yuan/mt compared to the previous trading day. The tight supply of primary lead smelters after the holiday has not eased. Smog weather in Henan temporarily affected spot trading and transportation, with individual suppliers quoting premiums of 100-150 yuan/mt against the SMM 1# lead average price. Due to reduced circulating supply, electrolytic lead in Hunan, Yunnan, and Guangdong regions maintained high premium quotations. Under the circumstances of elevated spot premiums, downstream buyers remained cautious, showing low enthusiasm for stockpiling, and market transactions appeared slightly sluggish.