This week, the total inventory of construction steel accumulated slightly. Rebar total inventory increased 2.4% WoW, and wire rod total inventory also rose 2.4% WoW. Currently, the market is in a policy vacuum period, with trading focus shifting to fundamentals. On the supply side, entering 2025, some steel mills previously affected by environmental protection-driven production restrictions have gradually resumed production, leading to an increase in pig iron output. EAF steel mills are expected to enter the holiday period successively in mid-to-late January, and supply will gradually decline thereafter. On the demand side, the market is currently in an off-season, with sluggish performance and weak overall transactions. Coupled with poor winter stockpiling expectations among traders, both upstream and downstream participants are operating cautiously. This week, the total inventory of construction steel increased slightly.

This week, rebar total inventory stood at 3.8817 million mt, up 90,800 mt WoW, an increase of 2.40% (previous value +2.12%). YoY, it decreased by 2.5144 million mt, a YoY decline of 39.31% (previous value -37.12%).

Table-1: Overview of Rebar Inventory

Source: SMM

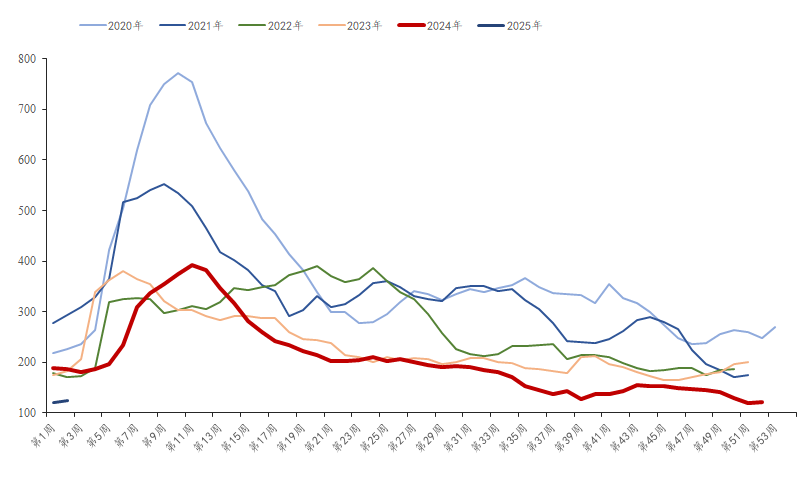

This week, in-plant rebar inventory reached 1.2507 million mt, up 42,300 mt WoW, an increase of 3.50% (previous value -0.12%). YoY, it decreased by 625,100 mt, a YoY decline of 33.32% (previous value -33.52%). Due to the completion of blast furnace maintenance at some steel mills and the gradual recovery of blast furnaces previously affected by environmental protection-driven production restrictions, pig iron output increased, slightly raising supply levels. As a result, in-plant inventory at steel mills increased slightly this week.

Chart-1: Rebar In-Plant Inventory Trends, 2019-2024

Source: SMM

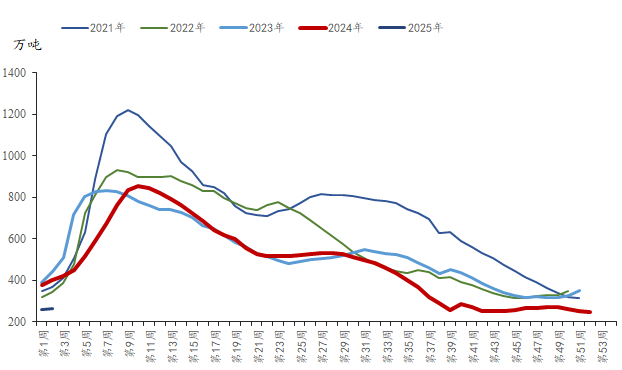

This week, rebar social inventory reached 2.631 million mt, up 48,600 mt WoW, an increase of 1.88% (previous value +3.2%). YoY, it decreased by 1.8893 million mt, a YoY decline of 41.80% (previous value -38.67%). Currently, the market remains in an off-season, with a sluggish trading atmosphere and poor winter stockpiling willingness among traders. Both upstream and downstream participants are operating cautiously, leading to a slight increase in rebar social inventory this week.

Chart-2: Rebar Social Inventory Trends, 2019-2024

Source: SMM

Overall, although pig iron output has increased, total production remains at a relatively low level. EAF steel mills are expected to successively enter their annual holiday period, resulting in relatively small supply-side pressure. On the demand side, as the Chinese New Year approaches, end-users are gradually halting operations, further weakening demand for construction steel. Coupled with poor winter stockpiling willingness in the market, rebar total inventory has accumulated. As the Chinese New Year approaches, market trading activity is expected to continue declining, and total construction steel inventory is expected to increase further next week.