》View SMM Aluminum Product Quotes, Data, and Market Analysis

》Subscribe to View SMM Historical Spot Metal Prices

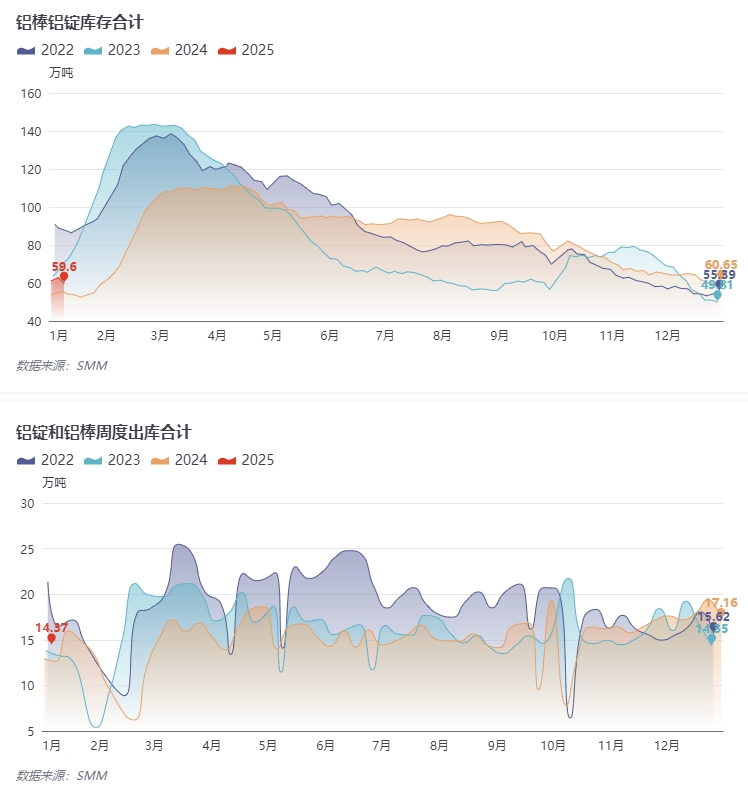

Mid-week, domestic aluminum ingot inventory saw a significant destocking against the trend, which undoubtedly exceeded most expectations.According to SMM statistics, as of January 9, 2024, the social inventory of domestic aluminum ingots stood at 459,000 mt, with 333,000 mt of domestically available aluminum inventory, down 36,000 mt from Monday and 28,000 mt from Thursday. Meanwhile, although SHFE aluminum appeared to be "lagging behind," the mid-week destocking undoubtedly supported and boosted aluminum prices. By today's close, the most-traded SHFE aluminum 2502 contract approached the 20,000 yuan mark, closing at 19,945 yuan/mt, up more than 300 yuan/mt from the intraday low.

Was the mid-week unexpected inventory performance an opportunity for recent aluminum prices or the "last frenzy"? Let’s first examine the reasons behind this rapid inventory decline:

(1) Insufficient price difference between primary metal and scrap, leading to increased substitution of aluminum scrap with primary aluminum.Currently, aluminum scrap circulation remains tight. Considering that aluminum scrap traders typically enter the Chinese New Year holiday earlier than downstream enterprises, scrap utilisation enterprises actively restocked, providing some support for aluminum scrap prices. Recently, the narrowing price difference between primary metal and scrap, coupled with the implementation of reverse invoicing policies, has led downstream users of aluminum scrap to switch significantly to pure aluminum. As a result, domestic aluminum ingot outflows from warehouses strengthened, reflecting downstream restocking of primary aluminum ingots at lower prices. This not only fulfilled the required primary aluminum stock but also replaced part of the aluminum scrap, ensuring raw material inventory for post-holiday production resumption.

(2) Limited mid-week arrivals created conditions for significant destocking.No further reductions in domestic aluminum billet supply have been reported, and casting ingot production in early January has not increased. Although Xinjiang shipments have returned to normal for some time, historical data shows that mid-week arrivals are generally limited. According to SMM surveys and warehouse feedback, arrivals are expected to increase after this weekend.

(3) According to SMM surveys, most downstream enterprises plan to start their holidays next week (January 14/15). Recently, downstream enterprises have been picking up goods in advance, building inventories at relatively low prices to reduce costs. Local traders have also accelerated outflows from warehouses before the holiday to clear inventory.However, there are regional differences in the spot market performance:

In east China, spot prices maintained small discounts during the week.Although PV manufacturers were actively restocking, recent production and operating rates were not ideal. The automotive sector performed well recently, but other industries showed weaker operating performance.

In central China, spot discounts narrowed and improved during the week.This was mainly due to the recent lifting of restrictions, which increased restocking demand from downstream enterprises. Spot trading was relatively active, and suppliers stood firm on quotes. However, the momentum for price support may not last, as new control measures are set to be implemented on the 10th.

In south China, with increased arrivals and expectations of downstream holidays, premiums narrowed rapidly.As traders put it, high spot premiums before the holiday were indeed unsustainable. Recently, especially for aluminum billets, traders have been "pushing volumes with discounts" to downstream buyers. Meanwhile, the destocking in south China this week was relatively small compared to east China, and overall inventory remained relatively stable.

Therefore, the supply pressure on domestic aluminum ingots before and after the Chinese New Year cannot be ignored. Although aluminum prices have been in a correction phase since December, which has exceeded expectations in driving spot outflows, the overall domestic aluminum demand remains in an off-season atmosphere. By year-end, some downstream enterprises have already entered or are about to enter holiday mode, and downstream purchasing interest may gradually decline. The likelihood of strong aluminum ingot outflows from warehouses in mid-to-late January is low. Compared to inventory data,the main driver of the current aluminum price decline remains the cost side—the anticipated collapse of the center of alumina futures and spot prices. Aluminum prices below the 20,000 yuan mark may become the norm during the pre- and post-Chinese New Year period.On the arrivals side, with Xinjiang shipments having normalized for some time, concentrated arrivals are expected to peak in the next two weeks, potentially increasing pressure on the spot market and reinforcing the inventory buildup turning point.SMM expects that despite the unexpected mid-week destocking, domestic aluminum ingot inventory will likely enter a continuous buildup phase later in January. By the eve of the Chinese New Year, domestic aluminum ingot inventory may build up to 500,000-600,000 mt.Closely monitor changes in downstream operating rates before the year-end holidays and the dynamic adjustments of the liquid aluminum proportion on the domestic supply side before the holiday.

Given that aluminum billet inventory buildup precedes aluminum ingot, observe the impact of aluminum billet inventory on overall domestic aluminum inventory.According to SMM statistics, as of January 9, domestic aluminum billet social inventory stood at 137,000 mt, continuing to build up by 2,900 mt from Monday and by 13,600 mt from last Thursday. Since the aluminum billet inventory buildup turning point on December 23, the weekly buildup rate has exceeded 10,000 mt.On the supply side, according to SMM's recently concluded December monthly survey on primary aluminum billets, domestic primary aluminum billet production in December declined but at a smaller-than-expected rate. In December 2024 (31 days), total domestic primary aluminum billet production was 1.465 million mt, down 12,000 mt MoM from November 2024 (30 days), a decrease of 0.81%; YoY, it increased by 162,000 mt, an increase of 12.4%. The domestic operating rate for primary aluminum billets in December was 56.4%, down 0.4% MoM. Entering early January, no further reductions in domestic aluminum billet supply have been reported, and arrivals remain ample. On a YoY basis, the gap with the same period last year widened further to 54,000 mt.

Due to the previous expansion of the Guangdong-Shanghai price spread, northern sources from Ningxia, Xinjiang, and Qinghai, in addition to the usual sources from Guangxi, Guizhou, and Yunnan in south-west China, have entered the south China market, causing the supply-demand pattern for aluminum billets to collapse. Processing fees have fallen rapidly and lack support. Consequently, regions like Wuxi and Nanchang, where processing fees remain relatively high, saw concentrated arrivals over the weekend. With the off-season atmosphere in the aluminum extrusion sector intensifying, aluminum extrusion operating rates remained weak, and pre-holiday restocking efforts were less than ideal. As downstream manufacturers enter holiday or pre-holiday mode, the domestic aluminum billet market may face an oversupply situation. Additionally, with significant improvements in Xinjiang shipments, there is a clear expectation of increased aluminum billet shipments to east and south China. With the continued concentrated arrivals of in-transit shipments,SMM expects domestic aluminum billet inventory to continue building up in January, potentially reaching 180,000-200,000 mt by the eve of the Chinese New Year.

Combining aluminum ingots and billets, the total domestic aluminum inventory currently stands at 596,000 mt, nearly 100,000 mt higher YoY. On a YoY basis, current domestic aluminum inventory is not in a favorable position. Although recent aluminum product outflows have outperformed the same period last year, the impact of recent aluminum prices and an earlier-than-usual Chinese New Year, leading to earlier downstream holidays, must be considered.Thank you to all our clients for your continued support of SMM in 2025. SMM will soon release a comparison chart of aluminum inventory before and after the Chinese New Year holiday. Clients in need, please stay tuned.